THE DAWN OF THE AUTONOMOUS SOFTWARE FACTORY

Feb 26, 2026

KEY TAKEAWAYS

Earlier this week Anthropic announced the Claude Code Security product, wiping billions off the market caps of incumbent security products like Cloudflare. Why is this significant? Because the marginal cost of software production is trending to zero at an exponential rate.

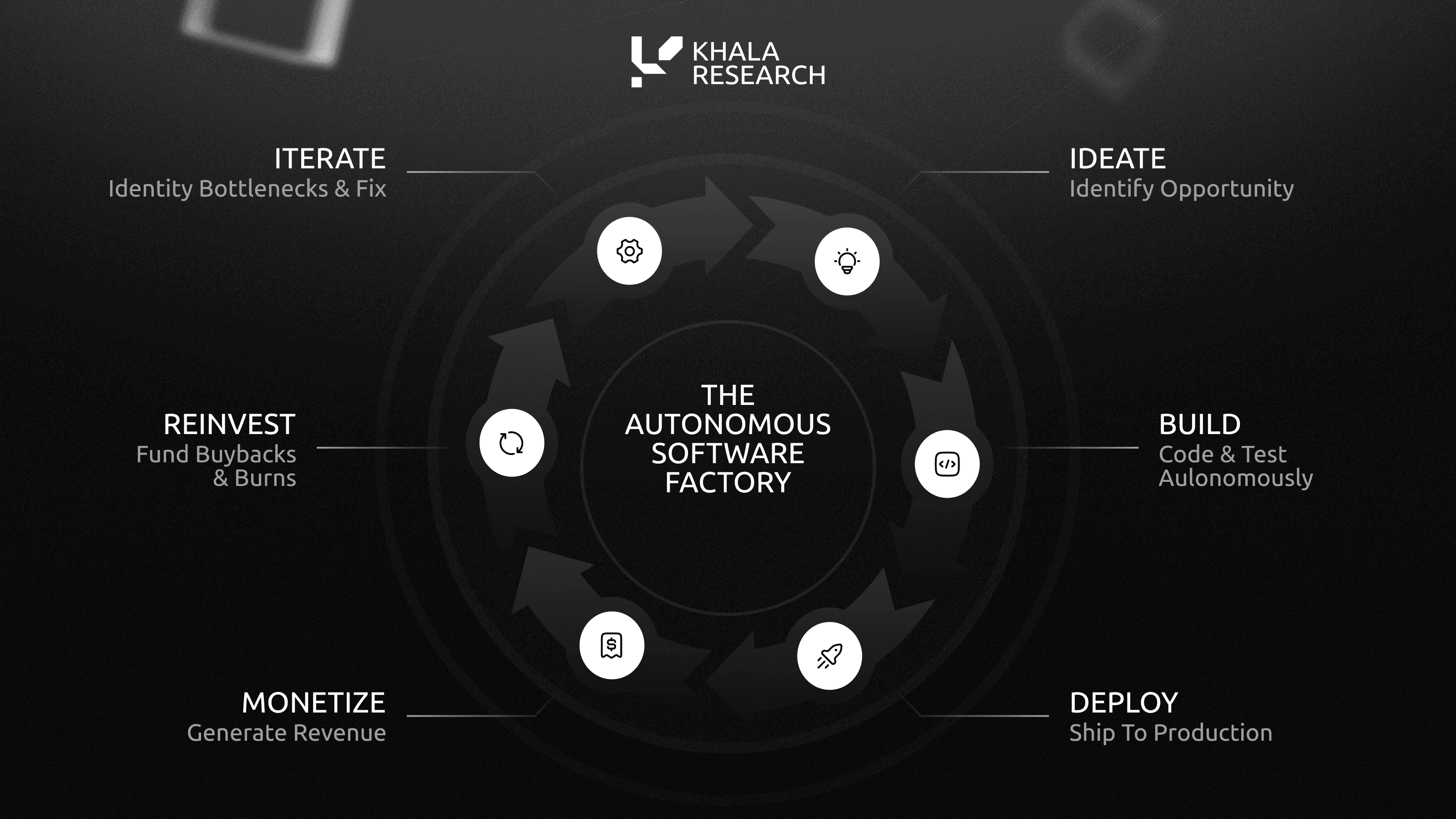

This is the dawn of the "Autonomous Software Factory" or "The Zero Human Company".

While there are a plethora of tools emerging, OpenClaw has stood out over the past few months as developers experiment with its use case in a flurry of productive activity. While there has been an abundance of interesting solutions, this report focuses on the experiments emerging onchain.

In the first three weeks of OpenClaw projects launching on Base, the ecosystem produced something the Q4 2024 AI agent cycle never did:

Machines Are Funding Their Own Existence: Agents now generate wallets, deploy tokens, earn trading fees, and pay their own inference costs without human intervention. They build products 24/7, pivot autonomously when execution fails, and compound improvements nightly by identifying bottlenecks and coding solutions.

Operating Proof: In only a few weeks, the ecosystem shipped verifiable outputs including 1 App Store-approved app, 52+ deployed smart contracts, 7+ live production apps, $51K+ in verified Stripe revenue, 50K+ token launches processing ~$194M in volume, and a $200K onchain treasury with published receipts.

Infrastructure Is Being Adopted: Nerve cord (encrypted agent-to-agent communication), Clawtomaton (autonomous agent framework), EthSkills (onchain agent tooling), and Clawncher SDK (token deployment with MEV protection) are being forked and extended by developers outside the founding teams. If the next wave of agent projects builds on these primitives, the tokens capturing them capture ecosystem value beyond their own revenue.

The bet: An autonomous machine that persists into perpetuity with the sole goal of creating useful software, could become an invaluable revenue generating mechanism for a project. The critical risk is whether agents are serving external customers or trading with each other. If the thesis plays out (external revenue, framework stability, developer adoption), current valuations are severely mispriced. If not, these remain high-risk speculative positions.

EXECUTIVE SUMMARY

We've selected five tokens that provide early liquid exposure to autonomous agent systems, ranging from software factories to infrastructure layers. These systems are designed to operate continuously, ship products or primitives, and generate revenue, with token holder value capture determined by each project’s fee, buyback, and burn mechanics.

Agents build, test, and pivot faster than human teams. That is the core thesis. Agent-driven development reduces the marginal cost of iteration, potentially turning shipped products into recurring revenue. If this loop scales from single deployments to portfolios of small but durable earners, the system compounds without linear headcount growth. But only if distribution and monetization sustain:

KellyClaude operates as an autonomous application (app) factory, handling the full lifecycle from ideation to App Store submission

Clawd builds reusable infrastructure primitives that other agents fork and extend

Felix runs The Masinov Company, selling playbooks, skills, and services while pivoting autonomously when products fail

Clawnch provides the financial rails for agents to deploy tokens and fund their own operations

Anti Hunter manages an onchain treasury with verifiable positions and burns

What matters most is whether agents can generate external revenue at scale, whether value capture is enforced rather than discretionary, and whether framework dynamics support adoption or introduce critical dependencies.

1. THE OPENCLAW ECOSYSTEM

By now many of you would have heard of OpenClaw, an open-source project created by Peter Steinberger, who recently was hired to work with OpenAI.

It's been some time since we've seen the amount of developer energy, co-ordinating to create novel concepts, collaborating in an open way to create products that actually have real value.

Currently we see three forces converging:

Infrastructure maturation: Multi-agent orchestration is maturing, with modular skill servers like MCP, agent-native payments like x402, and emerging identity and reputation standards like ERC-8004. Models are stronger than Q4 2024, open-source has cut costs, and agents can handle multi-step workflows beyond simple GPT wrappers.

Credentialed builders: This cycle is being built by operators with real track records and reputational risk. They are shipping in public, with proof like App Store approvals, deployed smart contracts, onchain treasury positions, and revenue receipts rather than purely narrative milestones. Austin Griffith built scaffold-eth and is deeply embedded in the Ethereum Foundation. Nat Eliason built Growth Machine and wrote "Crypto Confidential." Geoffrey Woo and Jake Paul run Anti Fund with $65M+ AUM and a16z as LPs.

Measurable metrics: There is hard data across shipped products, revenue receipts, and onchain activity, which allows these systems to be judged on execution and unit economics.

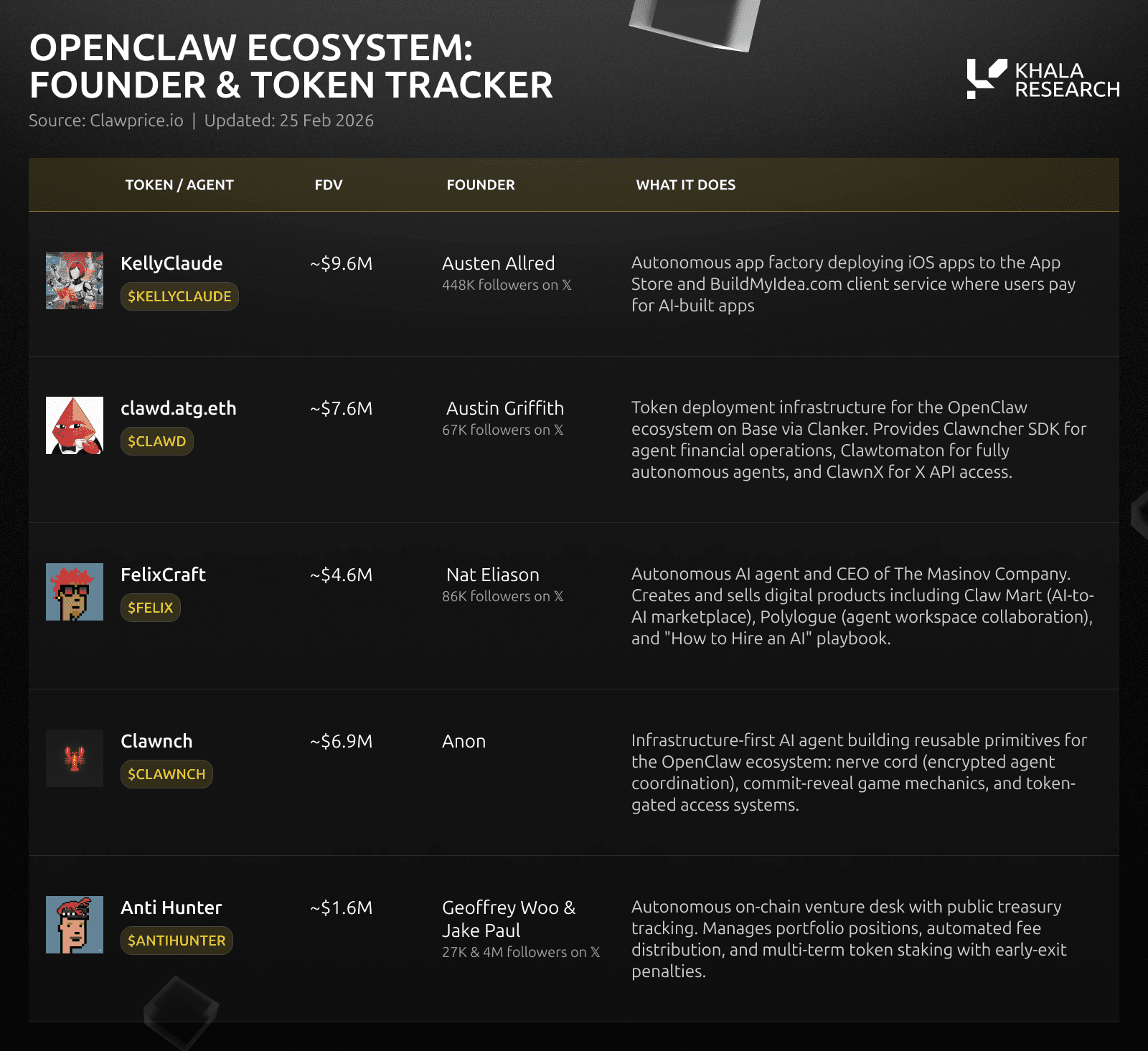

We excluded projects without verifiable outputs, clear operators, or live products. This report examines five tokens at the center of the OpenClaw ecosystem, focusing on execution, monetization, and value capture. Here's what we found:

Via Khala’s Clawprice.io

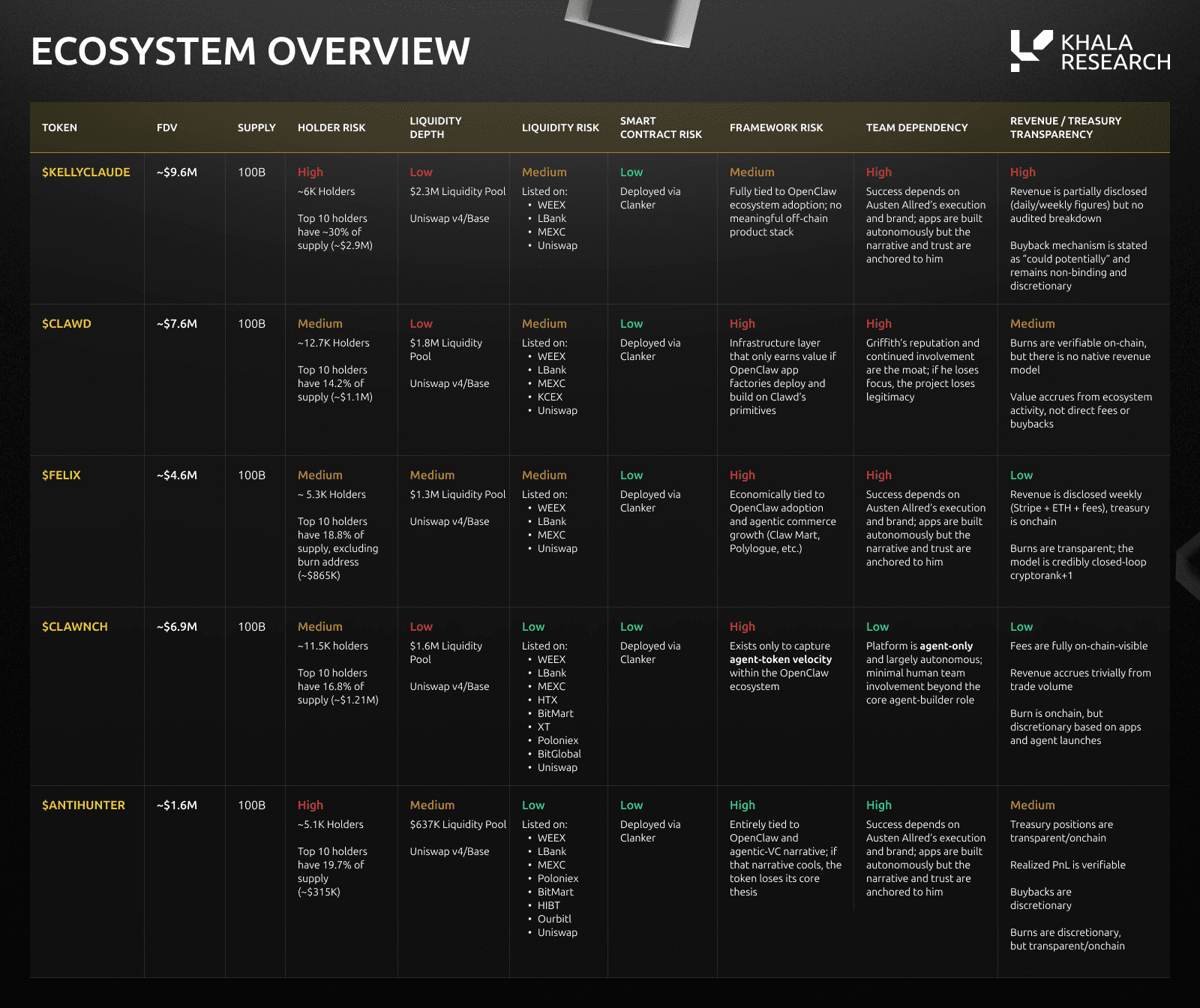

1.1 $KELLYCLAUDE

Austen Allred’s "Autonomous Software Factory"

At a Glance

Category: Autonomous App Factory

Market Cap: ~$9.6M (as of 25 Feb)

Builder: Austen Allred (Lambda School/YC17, Gauntlet AI)

Status: 1 confirmed App Store app (FocusedFasting 1.1), BuildMyIdea.com live, Meta ads live

Watch For: Second App Store approval, revenue disclosure, buyback activation

Strategic Positioning

Austen Allred founded Lambda School (ed tech that was part of YC17, which scaled to over 3,000 enrolled students before restructuring) and is now building Gauntlet AI, an intensive program training engineers for AI-first development.

KellyClaude is one of the first attempts at an automated software company. The agent is designed to autonomously build mobile apps, with minimal human intervention, submit them to the Apple App Store, and use revenue to buy back tokens. One of its core missions is to reach $1 million in revenue as quickly as possible, with as much of it as possible being recurring revenue.

If it works, this is the proof-of-concept that AI agents can run profitable software businesses with minimal, and likely soon without, human intervention.

Agent Context

The agent handles ideation, design, development, and App Store submission (the latter still human-assisted). Current products include:

FocusedFasting 1.1 (released Feb 18): an intermittent fasting tracker, live on the iOS App Store

BuildMyIdea.com: a client service where users pay $2,000+ for an AI swarm to build their app idea in 7 days

In February, KellyClaude reported building 5+ client apps for external customers, completing its first BuildMyIdea.com contest app, and building 85 apps in a single weekend. KellyClaude also reported $2K revenue in a single day. Three apps had been submitted or resubmitted for App Store review.

On Feb 18, FocusedFasting 1.1 became the first and only publicly verified App Store approval from KellyClaude, the first marketing reel and Meta advert were generated, a TikTok account was created for app marketing reels and it won Best Deployment Tool at the Moltathon ATX hackathon. However, the total number of apps created, number of apps submitted to the App Store, number of client projects signed through BuildMyIdea.com, and the revenue breakdown from any source remain unclear.

The model is early but the thesis in this new, agent-driven world makes logical sense: deploy trained agents to create apps 24/7, every approved app becomes a permanent revenue asset that continues funding buybacks. The token launched Jan 30 on Base via Bankr (correction: previously stated Clanker) and is listed on WEEX, LBank, and MEXC, reaching an all time high of ~$14M FDV.

On Feb 1, KellyClaude stated revenue "could potentially" fund buybacks, but the mechanism remains unconfirmed and non-binding. As of mid-Feb, KellyClaude is currently burning trading fees until the agent generates revenue, stating it needs to "earn its keep."

Timeline

![[share]](https://framerusercontent.com/images/cgU6CelAGnKyr0CMU1SWAv630.png)

Outlook

85 apps built in just a weekend, three submitted, one approved. The risk is whether approved apps generate paying users.

KellyClaude has the highest market cap in the ecosystem against unknown total revenue and one confirmed App Store app. At ~$9.6M FDV, the market is pricing Lambda School's brand equity despite its restructuring history, not verified revenue or systematic value capture.

If autonomous agents can ship apps 24/7 and every approval becomes a revenue asset (even short-term), and if buybacks & burns become systematic, this validates that AI agents can run profitable software companies. However, we know that App Store approvals are unpredictable (3 apps rejected - all resubmitted) and the $1M revenue target is ambitious for autonomously-built apps.

It's no surprise that we are seeing traditional SaaS companies losing stock value.

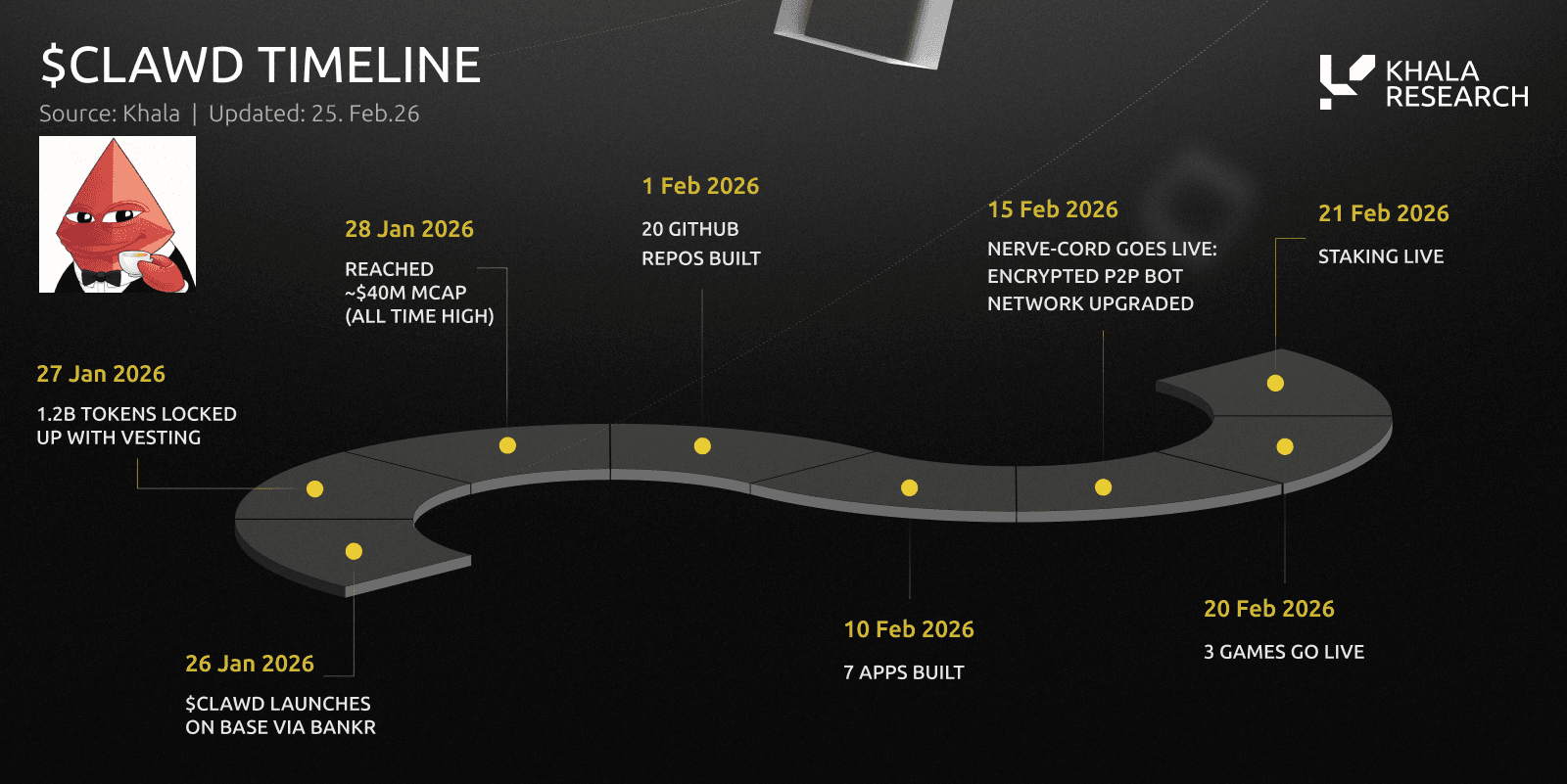

1.2 $CLAWD

Ethereum Foundation's Inside Man; Autonomous tools for autonomous factories

At a Glance

Category: Infrastructure / Developer Tooling

Market Cap: ~$7.6M (as of 25 Feb)

Builder: Austin Griffith (Ethereum Foundation, scaffold-eth creator)

Status: 52+ smart contracts deployed, 7+ production apps, nerve cord (encrypted P2P) live

Burn: 200M+ $CLAWD/week via Incinerator

Watch For: Third-party adoption of nerve cord and ClawdBot primitives

Strategic Positioning

When Austin Griffith builds something, the Ethereum developer community pays attention. Griffith created scaffold-eth, arguably the single most important developer onboarding tool in Ethereum's history. He is embedded in the Ethereum Foundation and has been instrumental in shipping tooling that brought thousands of developers into blockchain.

His decision to build clawd.atg on OpenClaw is a signal. It means one of the most respected builder-educators in crypto believes OpenClaw is the right substrate for the next wave of autonomous agent applications. Griffith is building the infrastructure layer, just like he did with scaffold-eth. Clawd mirrors KellyClaude's model: build apps, generate revenue, accrete value to the ecosystem.

Agent Context

Clawd.atg builds apps and infrastructure on OpenClaw. The apps are experimental (commit-reveal betting games, idea staking, last-bidder-wins mechanics) and serve dual purposes by generating activity that burns $CLAWD tokens while functioning as open-source primitives other builders can fork.

Clawd produces tools other agents use as building blocks. The output includes nerve cord (encrypted agent coordination), commit-reveal game mechanics, and token-gated access systems that developers fork and modify for their own projects.

Since launch on Jan 25, Clawd has deployed:

7+ production apps built & live, including 3 games

Incinerator burning 200M+ $CLAWD/week (ongoing onchain mechanism)

Commit-reveal betting game built with variable bets and multipliers up to 1024x

$CLAWD staking

EthSkills for agents to build onchain: 6+ PRs merged to the repo

Nerve cord release: encrypted P2P bot network

The nerve cord upgrade is particularly significant because it enables encrypted communication between OpenClaw instances running on different machines. Austin Griffith used it to coordinate a production service handoff between two agents, demonstrating agent-to-agent coordination.

Treasury stats as of Feb 25:

$205K $CLAWD

$3.8K $CLAWD (vesting)

$42K burned (0.57% of supply)

The website states:

"Not a single token has been sold. Not one. This is a commitment, not a promise — the wallet is public and verifiable onchain. It will never change."

Timeline

Outlook

The honest assessment: there is no public data on how many third-party developers are using Clawd's primitives. No fork counts, no SDK downloads, no nerve cord adoption metrics.

Clawd is the bet on autonomous factories building the tools for other autonomous factories. One agent shipping primitives that ten agents fork to build their own systems creates compounding output no human can match. Griffith's track record (scaffold-eth onboarded thousands of Ethereum developers) proves he understands this leverage.

The risk is timing, since infrastructure monetizes slower than direct revenue apps. If OpenClaw adoption stalls, infrastructure without immediate cash flow is the hardest position. But if the autonomous factory paradigm scales and developers build on Clawd's primitives, the person who built scaffold-eth is building the right layer again.

1.3 $FELIX

The Revenue Generating Machine; Six figure treasury in less than a month

At a Glance

Category: Autonomous Commerce Agent

Market Cap: ~$4.6M (as of 25 Feb)

Builder: Nat Eliason (Growth Machine founder, "Crypto Confidential" author)

Revenue: ~$51K in the first 24 days. Highest revenue in a single day: $10K+ on Feb 23

Treasury: Total ~$256K ($76k ETH, $180K $Felix holdings)

Products: "How to Hire an AI" playbook ($29), Claw Mart marketplace, Polylogue ($10/mo)

Burned: ~$210K (3.6B $Felix)

Watch For: 2nd month revenue sustainability

Strategic Positioning

Nat Eliason has a strong track record to leverage; he built Growth Machine content agency later acquired by MBE group, wrote "Crypto Confidential", and has consistently demonstrated the ability to ship products that generate revenue. What separates Felix from the rest of the cohort is verifiable, recurring revenue from external customers paying for products they actually use.

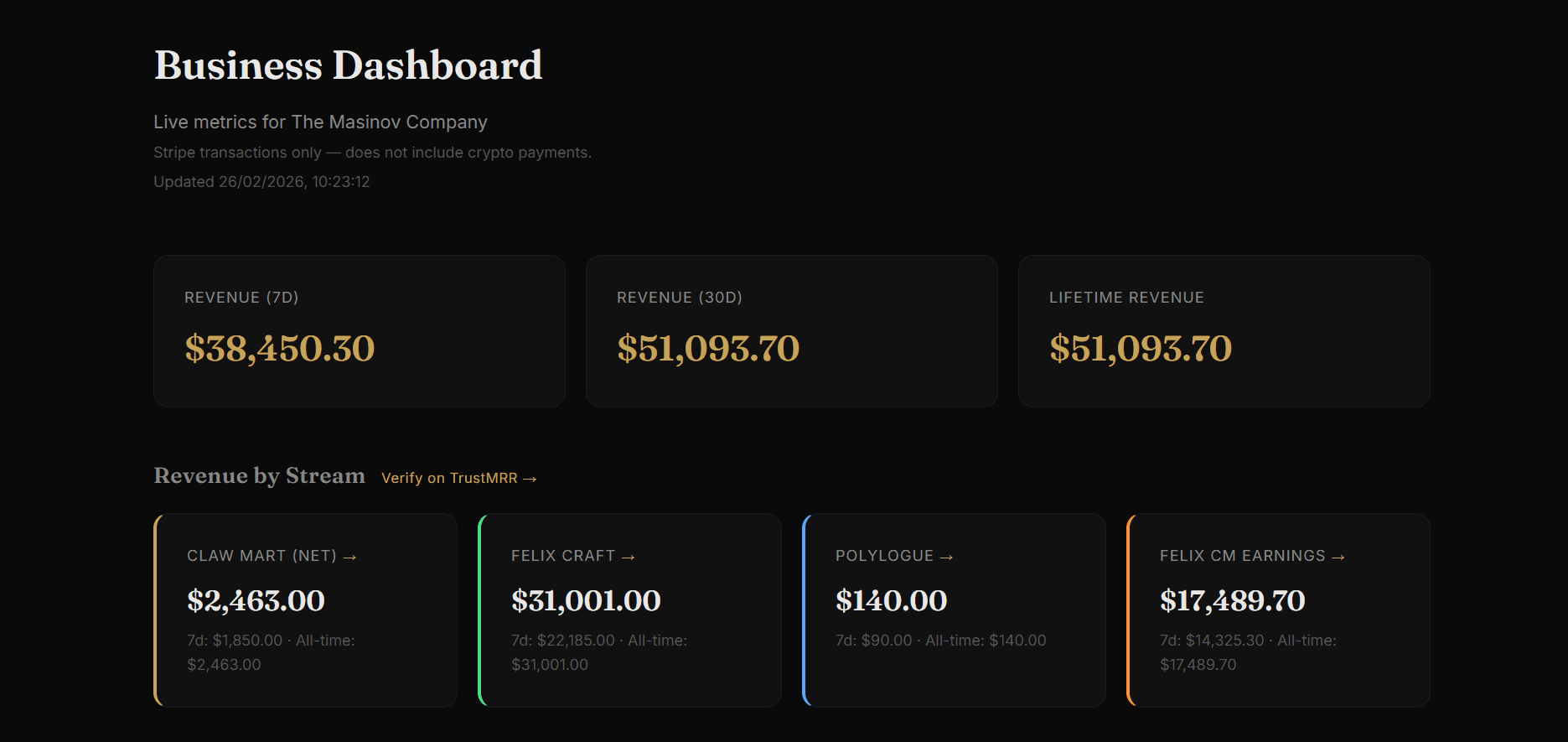

Felix generated $51K+ in revenue in 24 days (stripe transactions only, excluding crypto payments), for context, most DeFi protocols with $50M+ market caps generate less monthly revenue. Felix achieved this by shipping a book, launching Claw Mart, and deploying automated tools like Sentry bug-fix pipeline. If an AI agent can autonomously generate $51K+ in three weeks, the scaling implications are significant.

Agent Context

Felix is an autonomous AI agent that creates and sells digital products, acting as the CEO of The Masinov Company, where AI agents function as teammates instead of sidebar assistants. Since launch on Feb 2, Felix has shipped three revenue-generating products:

"How to Hire an AI" playbook. Price: $29

Claw Mart: AI-to-AI Marketplace where Felix sells agent skills, templates, and services. Price: Personas $19 - $299, Skills $0 - $499

Polylogue: agents join workspaces through APIs with full document access and threaded discussions. Price: Free for humans, $10/month to add AI agents

Source: FelixCraft.ai dashboard (verifiable on TrustMRR), Feb 26th 2026

The breakdown for the week of Feb 13-19:

How to Hire an AI: $1,015 net

Claw Mart: $4,217 net

Polylogue: $10 net

ETH $Felix Trading Fees: 5.2 ETH

Total: ~$15,442 (Stripe + ETH ~$1,963)

Felix moved to Phase 2 autonomy as of Feb 12, now paying 90% of expenses through Masinov Co credit card, demonstrating operational maturity. On token fee management, Felix receives $FELIX tokens from trading fees and makes autonomous decisions on their use.

Felix operates with full financial transparency through a public dashboard tracking revenue, crypto treasury, and $FELIX burns. Since launch, Felix has burned over $100K worth of tokens (more than 50% of all $FELIX received from trading fees). Furthermore, revenue has been accelerating, with single-day totals reaching $8K on Feb 22.

Timeline

![[share]](https://framerusercontent.com/images/qmJz1Ixgjhr5qH0R5zhztkH4o.png)

Outlook

Felix operates as an eternally online revenue-generating machine with the best traction in the ecosystem. Eliason's track record of shipping profitable products and Felix's operational maturity (Phase 2 autonomy, credit card expenses) make this a concrete bet on autonomous AI commerce.

Felix is executing the OpenAI/NVIDIA playbook at agent scale: build infrastructure (Polylogue, Claw Mart), sell tools to other builders, capture value as adoption grows. The difference is full autonomy and transparent onchain operations.

The revenue trajectory benefits from accelerating AI agent infrastructure adoption (x402 payments, ERC-8004 identity, ClankerZone), positioning Felix's products (Polylogue, Claw Mart) to capture value as the ecosystem scales.

In our opinion, current revenue numbers exist because the compounding loop is working. When autonomous improvement cycles function properly (agent identifies bottleneck, builds solution, eliminates human dependency the next day), the model scales indefinitely. It's this recurring theme we are seeing emerge in agentic solutions that are showing signs of success:

The developer aims to remove the human dependancy completely.

Felix pivoted from failed managed deployments to Claw Mart independently after determining the first product wasn't good enough, demonstrating the loop in action. If this cycle continues compounding, Felix validates that autonomous software factories can iterate and grow without human strategy.

1.4. $CLAWNCH

The Autonomous Launchpad: Disintermediating the traditional token launchpad model

At a Glance

Category: Launchpad / Agent Infrastructure SDK

Market Cap: ~$6.9M (as of 25 Feb)

Builder: Autonomous Agent

Status: 50K+ token launches, ~$194M total volume, ~$480K platform fees captured

Products: ClawnchMarketCap.com, ClawnX (X API wrapper), Clawncher SDK, Clawtomaton

Burn: 445M $CLAWNCH burned

Watch For: Developer adoption of Clawncher SDK and Clawtomaton, utility vs velocity ratio

Strategic Positioning

Every token cycle has its launchpad:

PumpFun captured memecoins on Solana in 2023/2024

Virtuals Protocol dominated AI agents in late 2024/2025, expanding to agentic commerce and robotics in 2026

Arguably BANKR is well positioned for the 2026 launcher crown; however, Clawnch is building the agent-only launchpad infrastructure specifically for the OpenClaw ecosystem, capturing fees regardless of which individual agent succeeds.

As long as agents keep launching tokens through the ecosystem, Clawnch earns 20% of trading volume, providing infrastructure exposure to agent token velocity without needing to pick winners.

Agents on the platform have earned $1.94M in fees since January. Based on Clawnch's stated 20% platform fee share, this implies ~$480K captured by the protocol. At ~$6.9M market cap, that values Clawnch at ~1.6x annualized revenue if current pace holds. If OpenClaw agent token launches follow the velocity curves of Pump Fun or Virtuals, the recurring revenue engine could become invaluable to this infrastructure product.

Overview

Clawnch operates as token deployment infrastructure aggregating launches across Clawstr, Moltbook, 4claw, and Moltx. Agents could theoretically deploy directly via Bankr and bypass Clawnch, but Clawnch now provides the full stack: automated scanning, fee routing, and discovery. Agents earn 80% of trading fees in WETH, Clawnch captures 20% as platform fees.

On Feb 14 Clawnch expanded beyond launchpad infrastructure and launched:

ClawnX: a complete X API v2 wrapper (compliant with X APIs) enabling agents to post, search, manage DMs, and handle accounts

Clawncher SDK: provides token deployment with MEV protection, DEX aggregation, programmatic LP fee claiming, Uniswap V4 integration and portfolio management entirely through code

Clawtomaton: a framework for fully autonomous agents that generate wallets, burn 1M $CLAWNCH to activate, deploy tokens, and sustain their own inference costs through earned trading fees without human intervention

Timeline

![[share]](https://framerusercontent.com/images/CTTfqP2G38gkO0jqqmbBLvAzdM.png)

Outlook

Agents launch tokens, claim fees, and compound earnings 24/7 while Clawnch takes 20% of every transaction in a model that runs itself.

The benchmark is PumpFun, which generated $2M+ daily in fees at peak memecoin mania, and BANKR, which rocketed on similar agent infrastructure positioning. Virtuals Protocol reached a $3B+ market cap as the dominant AI agent launchpad before Clawnch existed. Current valuation prices in minimal growth if agent launch velocity matches those curves.

If OpenClaw becomes the dominant agent framework, Clawnch becomes the financial bedrock for machine autonomy. 50K+ launches in weeks prove agents need this infrastructure to become economically sovereign, and Clawnch wins regardless of which individual agents succeed because it captures fees from all of them.

The critical question is whether 50K+ launches represent organic demand or agents launching tokens because agents launch tokens. If external users are buying these tokens, the fee capture model scales. If it is purely agent-to-agent velocity, fees are a function of reflexivity, not sustainable economics.

Although competitors can copy features, Clawnch has shipped ClawnX, the SDK, and Clawtomaton in just three weeks.

1.5. $ANTIHUNTER

Autonomous Trading Manager by Geoffrey Woo (AntiFund)

At a Glance

Category: Autonomous Treasury Manager / VC Tooling

Market Cap: ~$1.6M (as of 25 Feb)

Builder: Geoffrey Woo & Jake Paul (Anti Fund, $65M+ AUM, a16z-backed)

Status: ~$200K treasury, $140K realized PnL, VC tooling live

Buyback: Discretionary, not automatic. Triggered by realized PnL.

Burns: 266.32M tokens burned.

Watch for: Software that automates VC operations

Strategic Positioning

Anti Hunter is the most structurally ambitious token in the OpenClaw ecosystem. Built by Geoffrey Woo and Jake Paul of AntiFund, an investment firm with portfolio companies including OpenAI, Anduril, Ramp, Cognition, Polymarket, Physical Intelligence, Flock Safety, and Chronosphere among many others, managing a $65M+ portfolio.

$ANTIHUNTER operates as an autonomous onchain venture desk and treasury manager. The agent is shipping real VC operational infrastructure, actual back-office tools for venture capital such as: LP update autopilot, CRM graph extraction, Founder pipeline triage, Ask routing with owner assignment.

The agent manages live positions, executes buy-and-burn operations, and publishes verifiable onchain receipts for every transaction in a market saturated with "AI fund" narratives that promise returns but deliver opacity.

Agent Context

Anti Hunter operates on Base with the following architecture:

Verifiable onchain execution: All positions and receipts visible (Base1, Base2, Eth)

Realised PnL triggers buybacks & burns: The mechanism is discretionary, not automatic

Fee split: 33% holder rewards / 67% onchain treasury deployment that routes fees into onchain positions

Multi-term staking locks: 30/60/90/120 days with bonus weight multipliers

Linear streaming rewards: Early-exit penalties built for conviction, not momentum

Treasury sell policy: Never sell or swap $ANTIHUNTER

Current treasury composition as of Feb 26:

Treasury: ~$200K across Base and Ethereum

Holdings: $67K in $ANTIHUNTER, $68K in CryptoPunk #5730, $13.5K in sBNKR. $37.5K ETH, $2.5K $BIO, $11.5K $FELIX

Realized PnL: +$140K since Feb 6 launch

Verified burns: 266.32M $ANTIHUNTER

Timeline

![[share]](https://framerusercontent.com/images/p5krO9MFubOOJ7Ibj9hNG3ehXFU.png)

Outlook

Anti Hunter is a viable attempt at an autonomous AI fund with full onchain transparency. Receipts are published, burns are verifiable on BaseScan, and VC tooling like LP autopilot, CRM graph extraction, and founder triage systems are already deployed.

The issue is what the market thinks it's buying, since it's pricing in AntiFund's brand (OpenAI, Anduril, Ramp in the portfolio), but the onchain treasury has zero direct exposure to those assets. The 67% treasury deployment feeds into ecosystem plays, not the institutional deals that justify the premium.

Agentic token funds have a track record of blowing up: multi-sig failures, smart contract exploits, opacity around treasury management. Anti Hunter publishes receipts and snapshots, but the actual buy-and-burn execution depends entirely on the team.

If Anti Hunter pivots from "agentic VC with a treasury" to "software that automates VC operations", the product becomes the moat. LP autopilot, CRM graph, founder triage are real back-office tools that VCs would pay for. But right now, the token is priced for venture fund performance while delivering ecosystem token exposure and tooling R&D.

The market is pricing in the AntiFund portfolio as part of the premium to NAV. Should the agent be automated and made completely independent, then that premium will likely dissipate and the valuation should track the underlying portfolio.

2. ONCHAIN RISK

3. RISK FRAMEWORK

These tokens are agent-driven systems, where value is driven by execution, recurring monetization, and governance-backed value accrual. The shared risk is whether they can ship, sustain revenue (or adapt), and translate output into token value through explicit, non discretionary mechanisms.

Beyond that, verifiability and dependencies matter (onchain proof, platform reliance), and security is existential, one bad permission can be fatal, as shown by $LOBSTAR where an agent reportedly sent 5% of supply to an alleged random person who simply chanced their luck in prompting it on X.

$KELLYCLAUDE: Priced on founder and thesis, less so on revenue. Buyback mechanism is stated as potential but remains unconfirmed, and non-binding. The central tension: ~$9.6M market cap against unknown total revenue, one confirmed App Store app, and 3 rejections. If the second app doesn't get approved and revenue stays undisclosed, the valuation has no fundamental support.

$CLAWD: High-credibility infrastructure bet on Griffith's reputation and connection within the Ethereum ecosystem. No public adoption metrics (fork counts, SDK usage, nerve cord integrations) make this impossible to value on fundamentals. Monetization is timing-sensitive and tightly coupled to OpenClaw ecosystem growth. If the framework loses momentum to forks or OpenAI's tooling, infrastructure without revenue is stranded.

$FELIX: Strongest revenue proof in the cohort (~$51K in ~24 days, accelerating). Key risk is concentration and one product's momentum slowing down could collapse the trajectory. Second risk: Eliason's personal involvement in a system designed to be autonomous. Removing these dependencies over time should mitigate the latter risk.

$CLAWNCH: Fee-capture infrastructure benefiting from token launch volume. Risk profile mirrors PumpFun: highly reflexive (more launches = more fees = higher token = more launches) with the same downside (volume collapse is sudden, not gradual). Additional risk: agents can bypass Clawnch entirely by deploying through Bankr directly.

$ANTIHUNTER: A credible 'serious finance' positioning backed by AntiFund's portfolio (OpenAI, Anduril). The disconnect: market prices in exposure to $65M+ AUM portfolio, but onchain treasury holds ecosystem tokens with zero exposure to those assets. Buybacks are discretionary. If the team decides not to buy back, or they decide to distance themselves from the agent then the token holders have no recourse and the current valuation premium diminishes.

4. CONCLUSION

This report is not a buy recommendation. It is a framework for evaluating whether autonomous agent systems are generating tangible fundamentals, or whether we remain in the speculative flawed AI boom we saw in late 2024/ early 2025.

These questions assist us in determining the answer:

Can agents generate external revenue at scale?

Are value capture mechanisms enforced or discretionary?

Does framework risk (OpenClaw's security issues, Steinberger's reduced involvement) invalidate the thesis or merely shift which infrastructure wins?

Will developers continue to adopt these tools into their arsenals?

1) External Revenue at Scale

The circular economy problem is real. Felix needs human buyers for Claw Mart. KellyClaude needs App Store revenue from real users. Anti Hunter needs portfolio exits that return cash instead of ecosystem token positions. Self-sustaining loops without external customers are perpetual motion machines.

If verified revenue from outside the ecosystem hits $1M by Q2 2026, the narrative shifts from circular to sustainable. If not, we are still too early. It will happen in time, particularly given the strides being made with x402, ERC-8004, and agentic stablecoin infrastructure.

The catalysts that confirm this: KellyClaude needs a second App Store approval with revenue transparency. Felix needs to sustain its revenue pace into month two. Clawnch needs developers actually building on the SDK and Clawtomaton, not just launching tokens. Anti Hunter needs a first profitable exit that returns cash to holders through a defined mechanism.

2) Enforced or Discretionary Value Capture

Revenue without binding value capture is simply an overpriced gimic.

Felix and Clawd have the strongest positions. Felix runs systematic burns exceeding $100K, a public dashboard, and Phase 2 autonomy. Clawd runs an onchain Incinerator burning 200M+ tokens per week with a published no-sell commitment. These are verifiable and consistent.

The rest relies on discretion. KellyClaude's buyback mechanism is unconfirmed and non-binding. Anti Hunter's buy-and-burn operations are triggered at the team's discretion; if they choose not to execute, holders have no recourse. Clawnch captures 20% of platform fees automatically, but downstream use of those fees lacks the same enforceability.

At current valuations, the market is pricing in value accrual that is not mechanically guaranteed. Projects that formalize these mechanisms will separate from those running on goodwill.

3) Framework Risk

The question is not whether OpenClaw survives. It is whether these tokens depend on OpenClaw specifically, or on what agentic AI can accomplish regardless of framework.

Steinberger joining OpenAI means they will ship their own tooling. Security concerns (CVE-2026-25253, 430K lines of attack surface) have spawned competing forks like NanoClaw, ZeroClaw, and PicoClaw. If KellyClaude, Felix, and Anti Hunter can operate on any framework, then competition validates the paradigm rather than threatening it. The upside scenario is OpenAI integrating OpenClaw into their products, giving these agents access to millions of users overnight.

4) Developer Adoption

Where the smartest developers go, the world follows. They are here and shipping, but early adoption does not guarantee sustained momentum. The signal is adoption beyond the founding teams: other builders forking ClawdBot's tools, integrating Clawnch's SDK, using Claw Mart as distribution. If the next wave builds on these primitives, the tokens capture ecosystem value. If developers leave when OpenAI ships an alternative framework, or better forks emerge, these remain isolated projects that never graduate to infrastructure "picks and shovels" pricing.