XMAQUINA: ONCHAIN MARKETS FOR PRE-IPO ROBOTICS EQUITY

KEY TAKEAWAYS

1. Humanoid robotics is entering early commercialisation, with funding reaching nearly $14B in 2025 and combined valuations across leading companies exceeding $85B. Goldman Sachs projects a $38B market by 2035; Morgan Stanley sees $5T by 2050. No retail-accessible instrument offers tokenised, governable exposure to pre-IPO humanoid companies. Secondary platforms serve accredited investors only, applying illiquidity discounts of 10-30% and transaction fees of 3-5%.

2. XMAQUINA holds verified equity on the cap tables of six private humanoid robotics companies, with governance operating entirely through onchain proposals. The 1X position has appreciated 119% and the Apptronik preferred position 103% from cost base.

3. The DAO treasury holds $6.7M in robotics equity and $3.3M in cash. The DAO Portal reports a $28M headline that includes $18M in the DAO’s own untraded $DEUS at the Genesis Auction price (FDV of $60M). Whether that valuation represents a discount or a premium to NAV depends on which treasury baseline and supply assumption an allocator applies.

4. The Robotics Capital Markets (RCM) Protocol converts each verified equity position into a subDAO token paired against $DEUS. Trading fees flow to the treasury and each subDAO pairing creates demand for $DEUS as the intermediary asset. Whether the protocol compounds or the treasury stays static depends on sustained trading volume.

EXECUTIVE SUMMARY

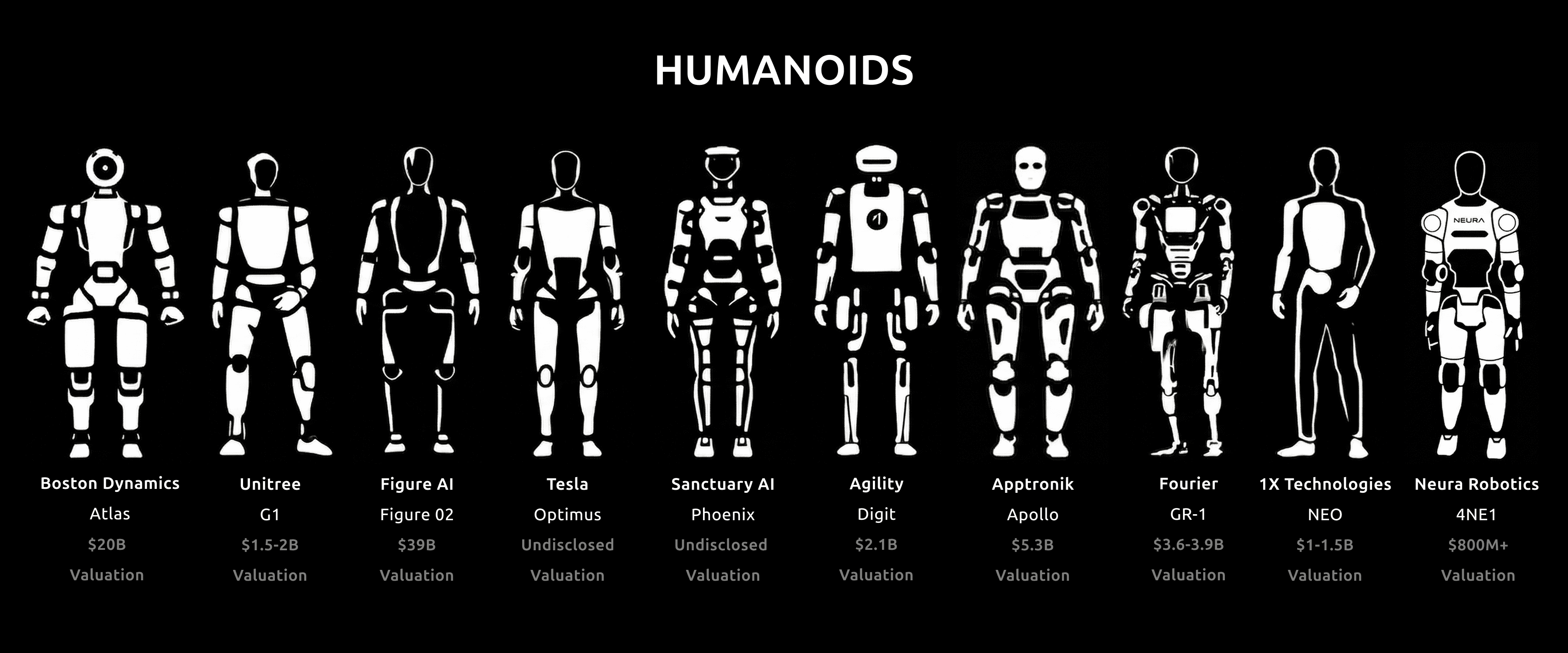

Private robotics equity has created tens of billions in value, but access remains structurally gated. Robotics startups raised nearly $14B in 2025, up 71% from 2024. The companies best positioned in the sector (Figure AI, Apptronik, 1X Technologies, NEURA Robotics, Agility Robotics) are years from IPO. Retail investors can access diluted exposure through public equities (Tesla, NVIDIA) or blended venture funds (ARK), but no instrument offers specific, governed exposure to named pre-IPO humanoid companies.

XMAQUINA's RCM Protocol is designed to capture that structural spread. Each equity position, held through a dedicated SPV, converts into a subDAO token paired against $DEUS on a DEX. Protocol fees flow to the treasury, funding new allocations and creating additional subDAO listings. The compounding case: fees grow the treasury, the treasury funds more equity positions, and new positions spawn new markets. The DAO's working treasury totals approximately $10M, with full composition detailed in Section 3.

This report covers the humanoid robotics market, the access problem, XMAQUINA's treasury and portfolio, RCM protocol mechanics and competitive positioning, $DEUS token economics including xDEUS staking, and a NAV premium analysis, followed by risk factors, catalysts, and a deployment framework.

Market capitalisations, protocol metrics, and token prices reflect data as of May 2026 and will change.

1. HUMANOID ROBOTICS

Humanoid robotics is shifting from a decade-long R&D cycle into early commercialisation, with real deployments replacing staged demos. Yole Group estimates 60+ active humanoid companies globally, with cumulative sector funding since 2017 exceeding $10B. Crunchbase data shows robotics startups raised nearly $14B in 2025, up from $8.2B in 2024, topping even the 2021 peak of $13.1B. Capital deployment has continued into 2026: Skild AI raised $1.4B in January, Apptronik raised $520M in February, EngineAI raised $200M in April, and NEURA Robotics is reportedly closing approximately EUR €1B (~$1.2B USD) backed by Tether.

Why Now

Adoption is showing up in unit numbers. Global humanoid output jumped from approximately 2,000 units in 2024 to 16,000 in 2025, with China representing over 80% of deployments. Projections exceed 100,000 units by 2027. Manufacturing cost per unit dropped approximately 40% between 2022 and 2023, from $50,000-$250,000 down to $30,000-$150,000. Unitree launched its R1 consumer humanoid at $5,900, later listing the unit on AliExpress, signalling early retail distribution infrastructure. Kia announced plans to deploy Boston Dynamics Atlas robots across its manufacturing facilities beginning in 2029.

Commercial deployment has replaced pilot programs at the leading companies. BMW has run Figure AI robots on daily 10-hour shifts at its Spartanburg plant for over 11 months, logging more than 1,250 runtime hours across 30,000+ vehicles. GXO Logistics deployed Agility Robotics’ Digit as one of the first humanoids in commercial warehouse operations. Toyota Motor Manufacturing Canada has signed a commercial agreement with Agility to deploy Digit across production facilities. Apptronik is running pilots with Mercedes-Benz, GXO, and Jabil, and holds an exclusive partnership with Google DeepMind on Gemini Robotics. 1X Technologies opened consumer pre-orders for its NEO robot at $20,000, with a $499 per month rental option and delivery expected in 2026.

Market Sizing

Analyst projections for the humanoid robotics market span a wide range reflecting different scoping assumptions. Goldman Sachs projects $38B by 2035, a figure revised ~6x from its prior $6B estimate, with 1.4M units deployed. Morgan Stanley’s broader estimate, which includes supply chains, repair, and support infrastructure, reaches $5T by 2050. Between those bookends, estimates from MarketsandMarkets, Barclays, and UBS range from $15B to $200B depending on scope and timeline.

The macro setup reinforces the demand thesis. Embodied AI changes labour cost structure the way software changed information cost structure. In the U.S., Deloitte and the Manufacturing Institute project 2.1M unfilled manufacturing jobs by 2030, at a cost of $1T annually.

The Access Problem

Leading humanoid companies carry reported or target valuations summing to approximately $85B across seven firms: Figure AI ($39B), Skild AI ($14B), 1X Technologies ($10B target), Unitree ($7B target), Apptronik ($5.3B), Physical Intelligence ($5.6B), and NEURA Robotics ($4B+ target). When these companies eventually list, the returns will have accrued almost entirely to institutional and accredited investors. No robotics-focused ETF captures pre-IPO companies.

Anthropic's pre-IPO implied valuation reached approximately $1.4T in May 2026, framing the scale of value accruing to private-stage AI companies before public market access. Figure AI issued cease-and-desist letters to brokers in 2025 to block unauthorised secondary trading of its stock; Anthropic followed in May 2026. Secondary platforms like Forge and Hiive serve accredited investors only, applying 10-30% illiquidity discounts with 3-5% transaction fees and multi-week settlement.

2. THE ROLE OF BLOCKCHAIN

Tokenising private equity addresses access through fractional ownership, programmable compliance, and near-instant settlement. But not all tokenised equity is real. The difference between legitimate tokenised exposure and a worthless claim comes down to asset verification and legal enforceability.

A proper SPV holds actual shares on the company’s cap table, with tokens representing fractional ownership of the SPV. Exit proceeds flow to token holders. An LP structure without asset backing sells tokens but may never acquire equity, leaving holders with a promise and no recourse if the operator collapses. For retail entering private robotics markets, this is the difference between owning verified equity and holding a claim that evaporates.

Platforms like BlackRock’s BUIDL fund, Securitize, and tZERO demonstrate how assets can be linked onchain to audited, legally enforceable holdings with custodial proof. On 17 March 2026, the SEC and CFTC jointly published an interpretation providing a token taxonomy and clarifying that most crypto assets are not themselves securities. For structures like RCM’s subDAO tokens, the investment contract analysis under Howey remains the relevant test.

Blockchain infrastructure adds three properties that traditional secondaries cannot: programmable compliance (transfer restrictions enforced at the contract level), fractional ownership (a $500,000 SPV position becomes accessible at any ticket size), and near-instant settlement (minutes versus the weeks required on platforms like Forge or Hiive). These properties change the access layer.

XMAQUINA’s RCM model requires proving each SPV holds shares on the target company’s cap table with enforceable claims.

3. XMAQUINA

A DAO-governed capital vehicle building onchain secondary markets for private humanoid robotics equity.

Mauricio, XMAQUINA co-founder, discussing XMAQUINA on the Supercycle Podcast

AT A GLANCE

Category: DAO-governed capital vehicle for private humanoid robotics equity

Market Cap: $60M FDV at $0.06 Genesis price (pre-TGE)

Treasury: ~$28M ($10M excluding $DEUS)

Equity Portfolio: $6.7M across eight positions in seven entities

Value Capture: 5% subDAO token supply allocated to DAO at launch; 1% trading fees; all subDAO pairs route through $DEUS

Risk: Pre-TGE token with unproven protocol revenue; 84% portfolio concentration in three pre-revenue companies

Watch For: $DEUS TGE; first RCM subDAO auction; monthly subDAO DEX volume; next portfolio company funding round or IPO filing

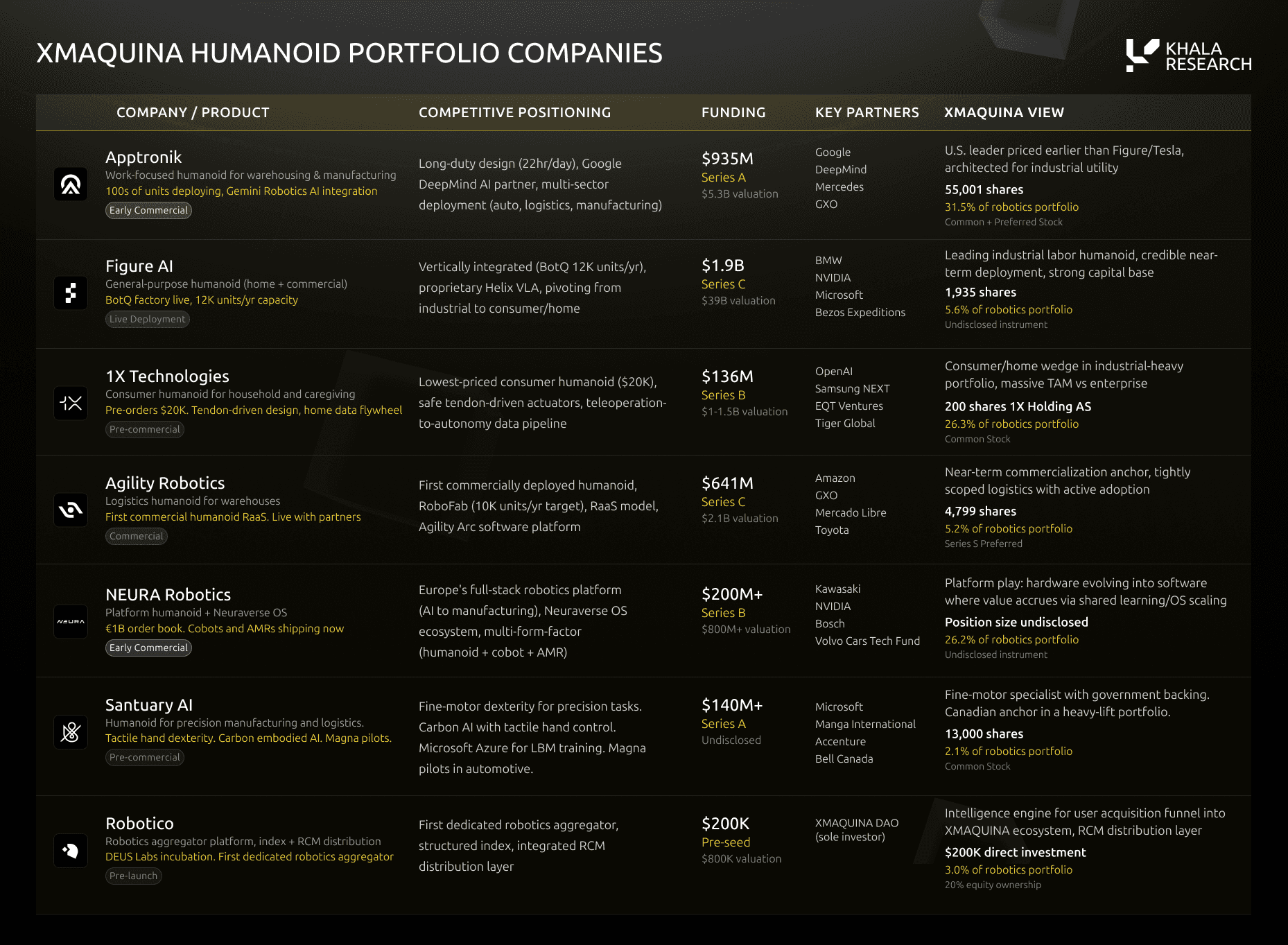

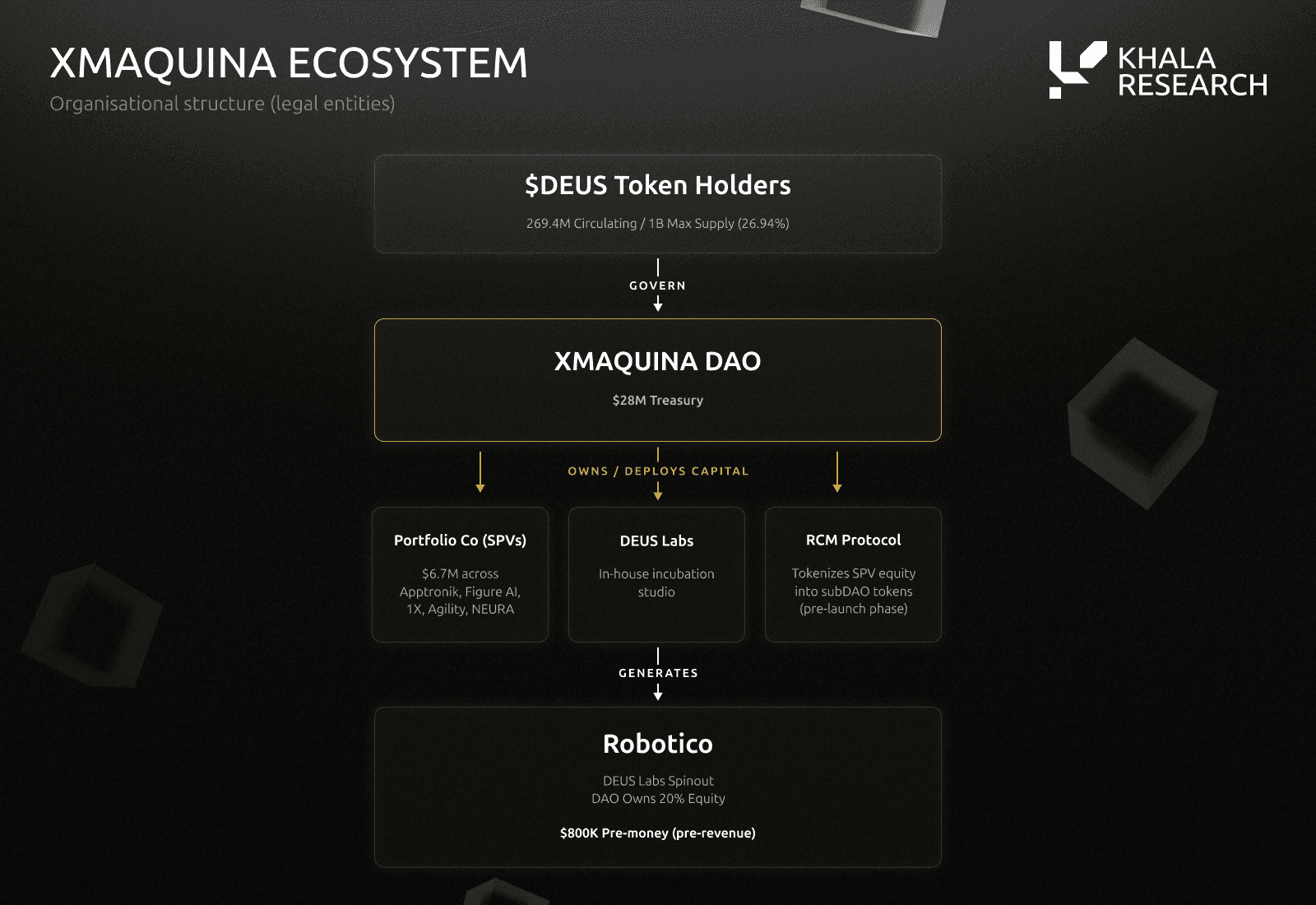

XMAQUINA launched in early 2024 to source and hold private robotics positions through a DAO-owned treasury where capital deployment is decided through onchain governance. The DAO raised $10M through five sold-out Genesis Auctions with approximately 1,860 holders, backed by Borderless Capital, Moonrock Capital, MH Ventures, Generative Ventures, Fundamental Labs, Waterdrip Capital, and strategic angels affiliated with Delphi Digital, Arkstream Capital, and KuCoin Ventures. To date, 15 governance proposals have been submitted through Snapshot, 14 of which have passed, averaging approximately 6.7x quorum. FDV stands at approximately $60M at the current Genesis Auction price of $0.06 per $DEUS.

The entity chain operates under a single governance layer. MachineDAO LLC is incorporated in the Marshall Islands as the DAO LLC, governed entirely by onchain $DEUS token voting. It is the ultimate beneficial owner and legal controller of all subordinate entities, with authority to appoint and remove directors. XMAQUINA Foundation Ltd. (Cayman Islands) serves as the off-chain execution arm, holding legal title to equity on behalf of the DAO and executing investments only upon governance approval. RWA Robotics Ltd. (BVI) is a limited-purpose entity for $DEUS token issuance and SAFT execution.

Treasury Composition

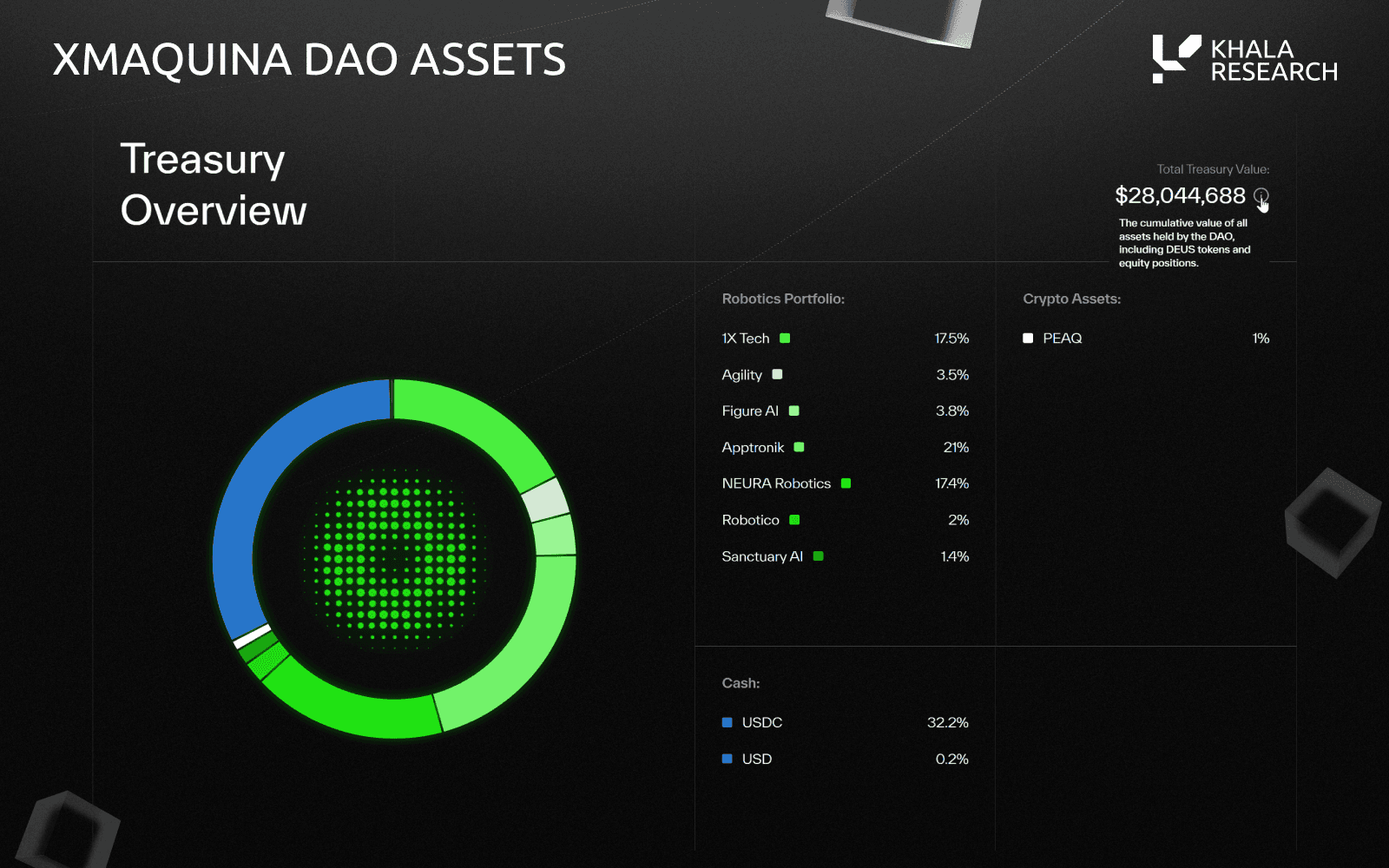

As of May 2026, the DAO Portal reports total treasury value of $28M.

Source: XMAQUINA DAO Portal, May 2026. Live dashboard; figures update in real time.

Treasury Composition Note: The $18.1M in crypto assets on the DAO Portal consists of 300M $DEUS tokens valued at the $0.06 Genesis Auction price ($18M) and 3.7M $PEAQ tokens (~$100K). The PEAQ was received as payment during Genesis Wave 1, which accepted PEAQ exclusively. The $DEUS represents the DAO Treasury allocation, governance-locked and deployable only through onchain vote for liquidity provisioning, staking incentives, or token sales to fund operations and equity acquisitions. Since $DEUS has not yet launched on a public exchange, the $0.06 valuation reflects auction pricing rather than market clearing. This is standard for pre-TGE DAO treasuries. For NAV analysis, the headline $28M includes these tokens; the working treasury (robotics equity plus cash) is approximately $10M. Both frameworks are presented in Section 3.2.

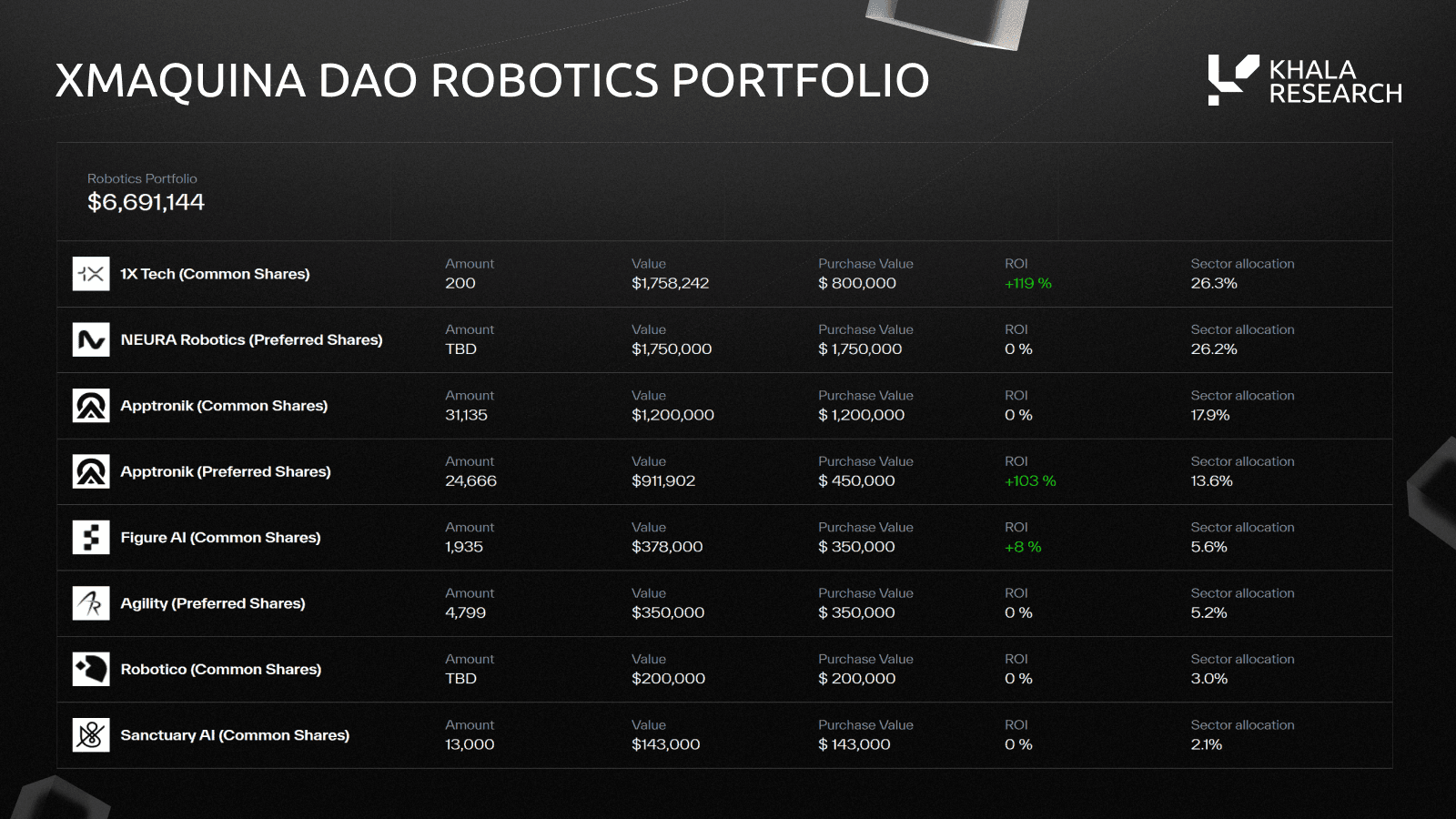

Robotics Portfolio

The portfolio totals $6.7M across eight positions in seven entities, deployed at approximately $5.2M cost.

Source: XMAQUINA DAO Portal, May 2026.

Attestation letters from Andersen LLP are published on the XMAQUINA docs page, covering six allocations: Apptronik (BOT-01), Figure AI (BOT-03), Agility Robotics (BOT-04), Apptronik follow-on (BOT-06), 1X Technologies (BOT-07), and NEURA Robotics (BOT-09). The two Apptronik positions represent separate governance-approved deployments at different entry points.

Portfolio Company Profiles

Apptronik builds Apollo, an AI-powered humanoid designed for manufacturing and logistics. The company raised $935M total at a $5.5B valuation in its February 2026 Series A extension, with Google, Mercedes-Benz, John Deere, and the Qatar Investment Authority participating. It holds an exclusive partnership with Google DeepMind on Gemini Robotics and is running pilots with Mercedes-Benz, GXO, and Jabil. Apollo is designed for 22-hour daily operation with hot-swappable batteries. The DAO holds two separate positions totalling 55,801 shares: 24,666 preferred (acquired at $450,000, now +103%) and 31,135 common (acquired at $1,200,000, currently flat). Combined Apptronik exposure: $1,650,000 deployed, 31.5% of portfolio, making it the largest company-level allocation.

1X Technologies is building NEO, a consumer humanoid priced at $20,000 with a $499/month rental option. The Norwegian company relocated to Palo Alto in 2025 and has been testing NEO in several hundred homes. In January 2025, 1X acquired Kind Humanoid, adding the team behind the Mona bipedal humanoid. Total funding stands at $136.5M across 10 rounds. The DAO’s shares were acquired at a reported $4.55B valuation. Crunchbase confirms a new Series B round closed on 27 February 2026 listing a single investor with no disclosed valuation, which appears to be a small extension rather than the previously reported $10B+ raise. On the secondary market, 1X shares trade at approximately $2,163 per share on Hiive, as of May 2026. The DAO holds 200 common shares (acquired at $800,000, +119%, 26.3% of portfolio).

Figure AI develops general-purpose humanoids for industrial and home environments. Its Figure 02 completed an 11-month deployment at BMW's Spartanburg facility before retiring in late 2025. Figure 03, announced October 2025, is the current production model designed for mass manufacturing. Figure operates BotQ, a vertically integrated manufacturing facility producing over 350 units with throughput ramping to one per hour. The company raised over $1B in its September 2025 Series C at a $39B valuation, led by Parkway Venture Capital with NVIDIA, Brookfield, and Intel Capital. The DAO holds 1,935 common shares ($350,000 deployed, +8%, 5.6% of portfolio).

NEURA Robotics is a German company developing cognitive humanoids and the Neuraverse operating system for fleet-wide skill sharing. NEURA has partnerships with Schaeffler, HD Hyundai, and GFT Technologies and has reported €1B in orders, with Amazon deploying NEURA cognitive robots in fulfilment centres. NEURA has raised €185M in total confirmed funding across five rounds, with the latest closed round being a €120M Series B (January 2025, led by Lingotto). Bloomberg reported in March 2026 that NEURA is raising approximately $1.2B backed by Tether at ~$4.3B (€4B). The company acquired EK Robotics, a 300-person industrial automation specialist, in October 2025. The DAO’s position: $1,750,000 (26.2% of portfolio).

Agility Robotics develops Digit, a bipedal warehouse robot and the first humanoid with commercial workplace safety approval. Digit is deployed at GXO, Amazon, and Toyota facilities. The company operates RoboFab, a 70,000 sq ft facility targeting 10,000 units per year. Agility has raised approximately $680M in total funding at a reported $1.8B valuation. The DAO holds 4,799 preferred shares ($350,000 deployed, 5.2% of portfolio).

Sanctuary AI develops Phoenix, a general-purpose humanoid designed for fine-motor labour tasks across manufacturing and logistics. The company focuses on "Carbon," an embodied AI system paired with tactile hand dexterity for precision operations. Phoenix has been tested with Magna International in automotive plants and holds a strategic alliance with Microsoft. To date, Sanctuary has raised over $140M with investors including BDC Capital, Accenture, Magna, Verizon Ventures, and Workday Ventures, alongside a $30M Strategic Innovation Fund contribution from the Government of Canada. The DAO holds 13,000 common shares ($143,000 deployed, 2.1% of portfolio).

Robotico is DEUS Labs' first incubation, a market intelligence platform tracking companies, robots, and capital flows across the embodied AI sector. The platform catalogues 95+ humanoid models, real-time stock tickers for robotics-adjacent public companies, funding round tracking, valuation data, and weekly intelligence reports. The DAO acquired 20% equity at $800K pre-money as the sole pre-seed investor, deploying $200K (3.0% of portfolio).

Portfolio Risk Observations

The top three positions (combined Apptronik 31.5%, 1X 26.3%, NEURA 26.2%) represent 84.0% of the robotics portfolio. The portfolio is 100% Western (US, Norway, Germany), despite China deploying over 80% of global humanoid units in 2025. Every portfolio company uses the NVIDIA stack for simulation and training. Two depend on exclusive AI lab partnerships (Apptronik/Google DeepMind, 1X/OpenAI). Exit decisions are governed by xDEUS holders through onchain proposals. Following an exit, governance may vote to distribute up to 40% of realised proceeds to active xDEUS stakers, with the remainder retained in treasury for new allocations. RCM-linked SPV positions settle at the SPV level.

Deal Sourcing Pipeline

The DAO's Northstar Council has identified additional targets including FieldAI (confirmed), Skild AI, Physical Intelligence, Clone Robotics, RoboForce, AgiBot, Unitree, and Sunday Robotics. The roadmap targets 10 treasury allocations by Q3 2026. Pipeline activity feeds the treasury growth thesis: more positions mean more subDAO markets, more protocol fees, and a broader portfolio base.

3.1 ROBOTICS CAPITAL MARKETS (RCM)

Infrastructure that brings private robotics equity onchain, creating always-on, permissionless markets around verified positions.

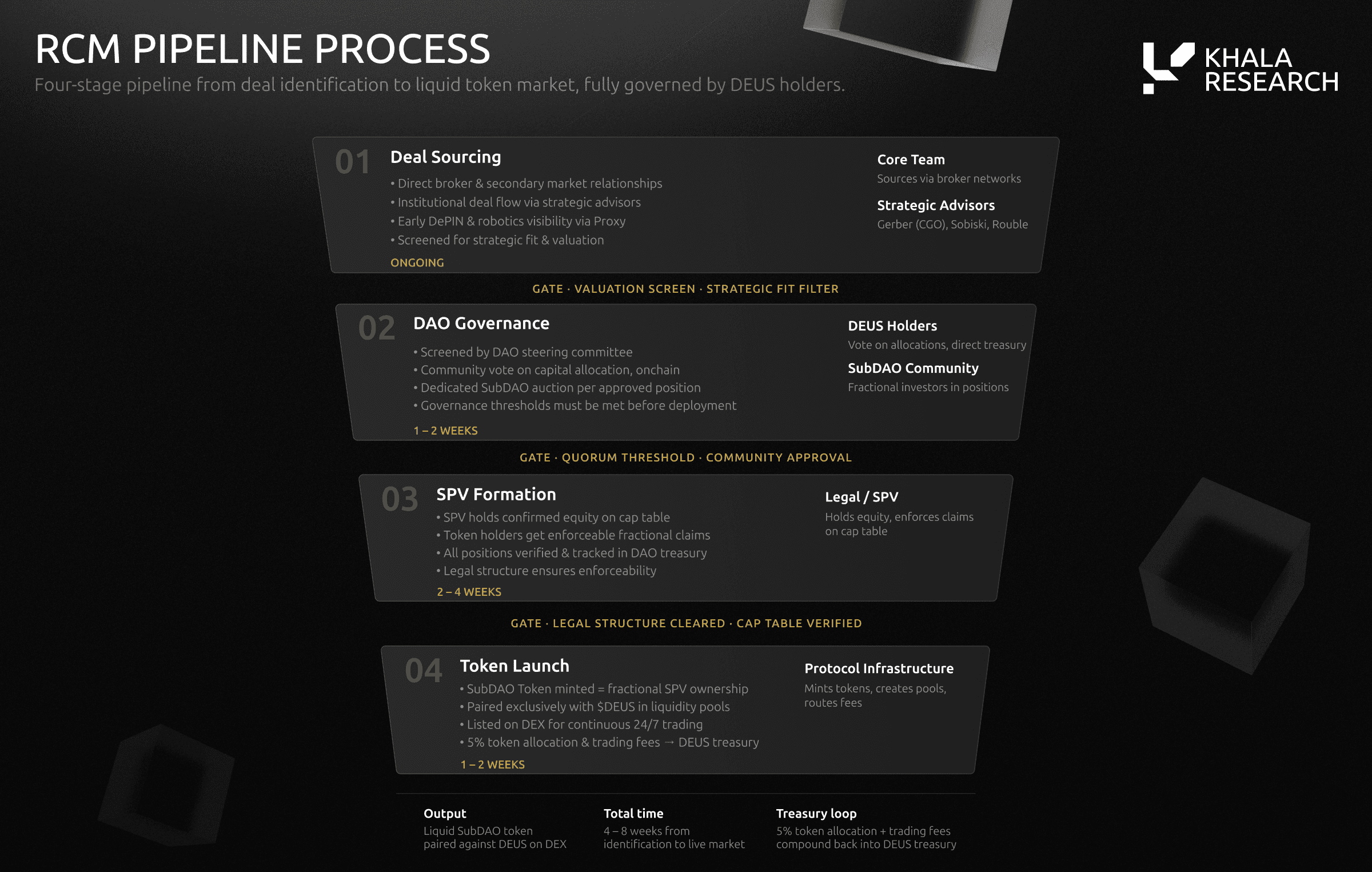

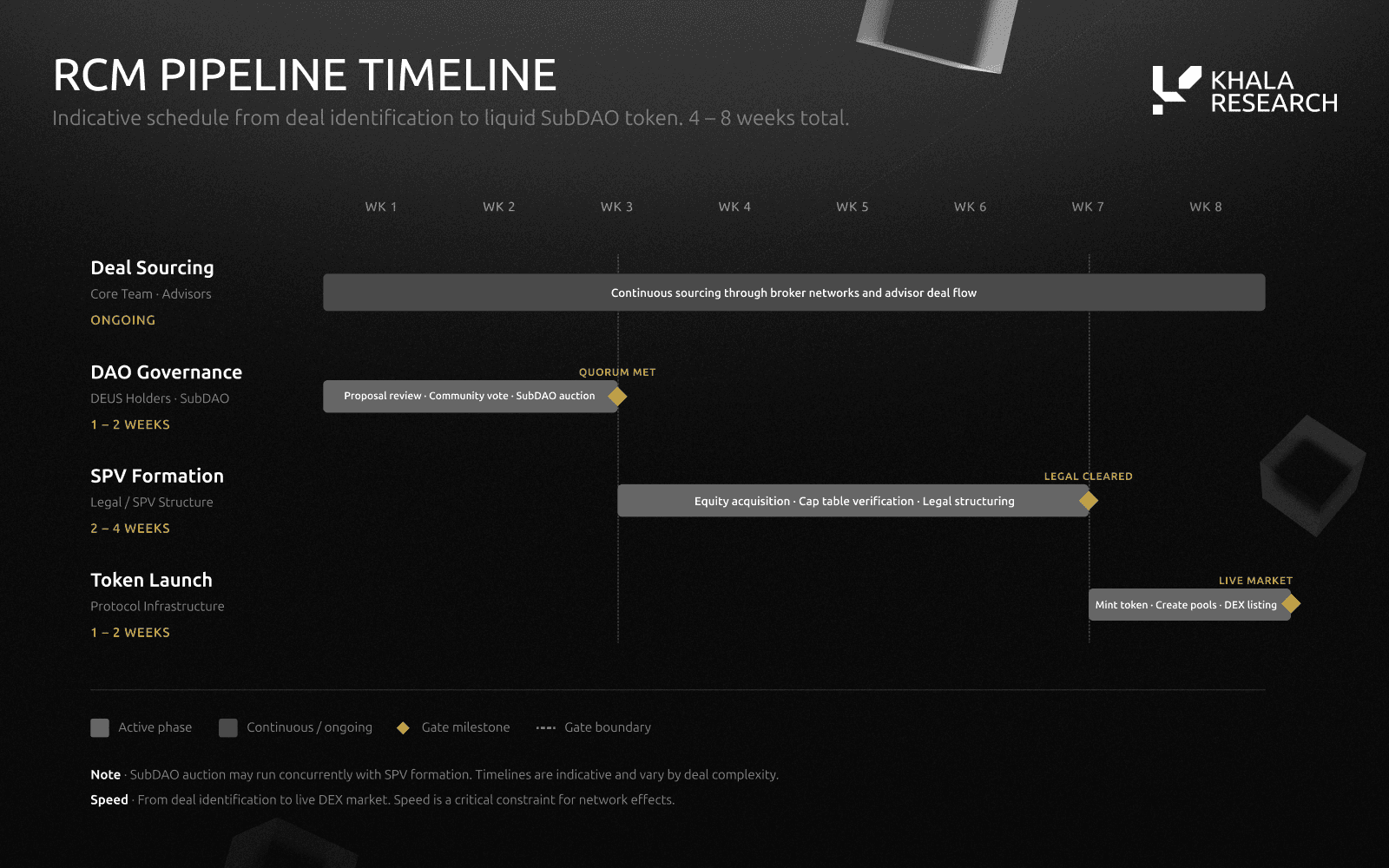

To move beyond a treasury-only model, XMAQUINA is launching the RCM Protocol. Governance proposal XMQ-03 (RCM Protocol Development) passed with 152 votes at 601% quorum. The roadmap targets a Q2 2026 rollout, with initial governance proposals defining the first asset allocations and the first RCM SubDAO auctions brought onchain, progressing through to the full protocol launch in Q3 2026. An expansion phase (perpetuals, prediction markets, new listings) is planned for Q4 2026.

How RCM Works

The team sources opportunities through direct relationships with brokers, seed investors, and secondary platforms. Strategic advisors include Michael Ganser (former CEO of Cisco Germany), Lex Sokolin (Generative Ventures), and Ruben Portela (Wise3 Ventures), Simon Dedic (CEO, Moonrock Capital), and Alvaro Gracia (General Partner, Borderless Capital). The DAO integrates with peaq for visibility into robotics and physical AI projects.

The pipeline operates in four stages: XMAQUINA sources an allocation; the community raises capital via a subDAO auction; a dedicated SPV is formed to hold confirmed equity on the cap table; a subDAO token is minted, paired against $DEUS, and listed on a DEX. Total time from deal identification to live market: 4-8 weeks.

SubDAO tokens enable 24/7 trading exposure to SPV-held positions without accreditation or broker intermediaries. A $500,000 Figure AI position becomes tradable as a subDAO token (eg: $dFIGURE) on a DEX, introducing price discovery for private equity. During normal operation, the token trades freely on secondary markets against $DEUS, with price discovery determined by market supply, demand, liquidity depth, and available information. The market price may trade at a premium or discount to the implied NAV of the underlying SPV position. Token holders do not hold equity in the underlying company, hold shares in the SPV, or receive dividends. Any value subDAO tokens accrue is entirely market-driven and may not reflect the valuation of the associated SPVs. This is a coordination and sentiment instrument, not a tokenised security.

At a liquidity event (IPO, acquisition, or other exit), the SPV realises proceeds from the underlying asset. The current framework assumes a Reg S structure, meaning US persons are excluded from the subDAO token offering and redemption process. Eligible non-US holders who complete KYC/KYB can redeem or claim proceeds according to the applicable token terms. The XMAQUINA treasury does not absorb exit proceeds. Settlement occurs at the SPV level. The team has advised us that a full redemption and settlement framework will be documented prior to RCM Protocol launch.

Equity positions are executed through SPVs administered by Tier 1 regulated secondary market operators including Forge Global, Hiive, EquityZen, and Zanbato, all SEC-registered broker-dealers and FINRA/SIPC members. SIPC coverage protects up to $500K per account against broker-dealer insolvency at the platform level.

Revenue Model

RCM generates revenue through two mechanisms, as described in the RCM blog post: each subDAO allocates 5% of its token supply to the XMAQUINA DAO at launch, and ongoing trading fees from DEX activity flow to the treasury. Governance proposal XMQ-03 established a 1% protocol fee on subDAO trading. Governance directs these flows toward new robotics equity acquisitions, $DEUS buybacks, or staking incentives.

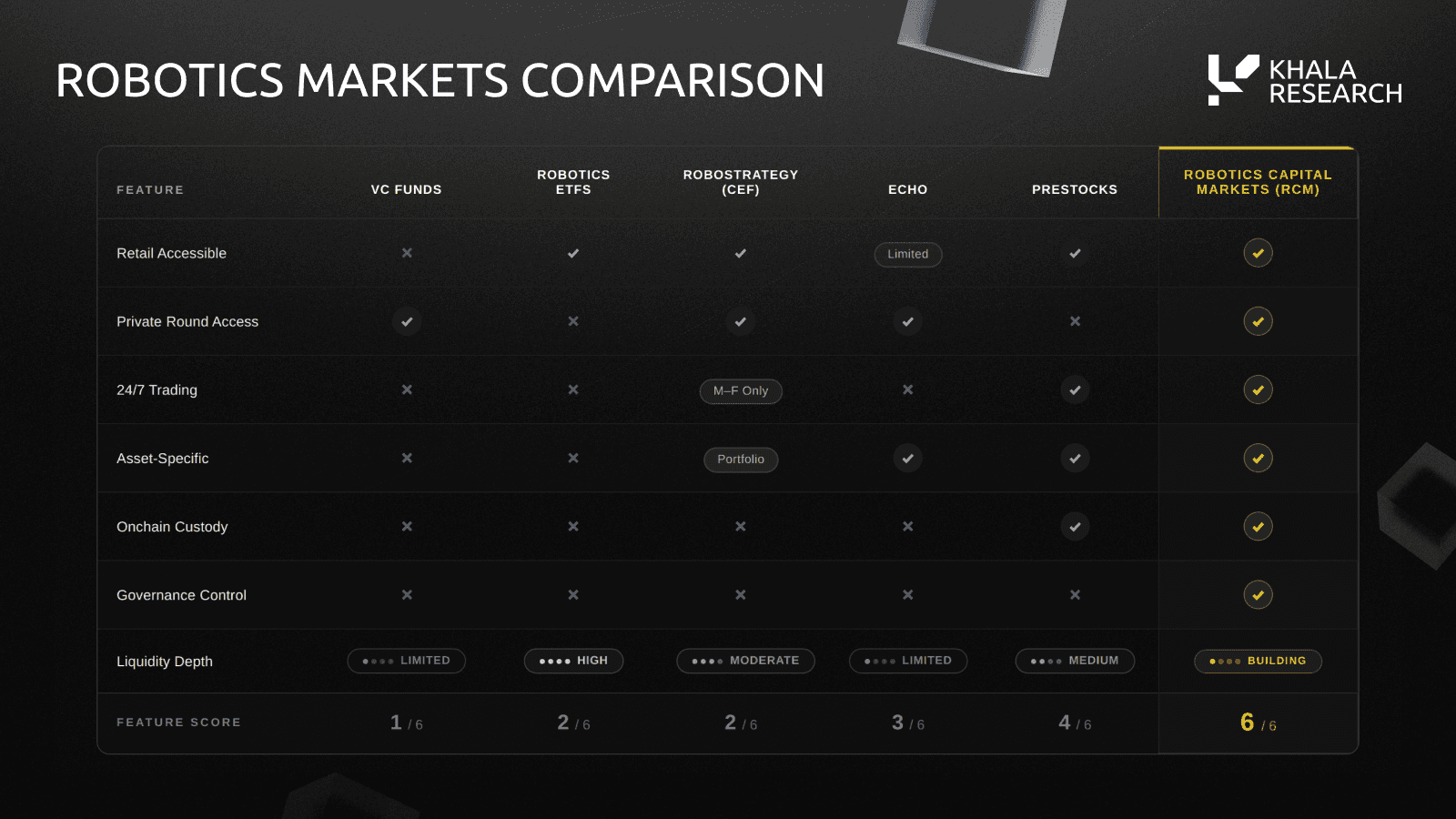

Competitive Positioning

RoboStrategy already proves the model works in TradFi. A closed-end fund registered under the Investment Company Act of 1940, it listed on Nasdaq under ticker BOT in May 2026 with a portfolio spanning more than 12 robotics and physical AI companies including Figure AI, Apptronik, Dyna Robotics (where it led the $120M Series A alongside CRV and First Round Capital), Standard Bots, and Dexmate, with monthly NAV and quarterly SEC disclosure.

It gives institutional and retail investors access to private-stage robotics through a listed, regulated vehicle. The trade-off is limited redemption windows, quarterly pricing, and active management by FP Strategies LLC. Most closed-end funds trade at persistent discounts to NAV. BOT is an exception. Listed on May 11, 2026 at a private offering price of $10.00 per share, the stock has already traded between $19.20 and $59.00. Against the most recent disclosed NAV of approximately $7.34 per share (from February 28, 2026 net assets of $146.2M and 19.9M shares outstanding), that implies a premium ranging from roughly 160% to 700%. The May 15 close of $36.01 sits near the middle of that range at approximately 390%.

Where BOT is a passive portfolio with no compounding mechanism, RCM claims to offer a different structure: 24/7 DEX trading, no minimum investment, governance-directed fee flows, and a revenue flywheel where protocol fees fund additional equity acquisitions. Whether that structure can sustain a comparable premium depends on volume and execution.

XMAQUINA cites Pump.fun and Virtuals Protocol as design inspirations. Pump.fun demonstrated automated liquidity and frictionless token creation, generating approximately $1B in lifetime revenue across 18M+ tokens. Virtuals Protocol has evolved beyond a launchpad into a broader coordination layer for AI agents. Its aGDP framework measures total economic activity generated by AI agents across the ecosystem, and the protocol is expanding into agentic commerce and robotics. With over 18,000 agents deployed, $13.8B in cumulative DEX volume, and $70M in cumulative revenue, Virtuals has built the most developed model for tokenised conviction markets around specific projects.

RCM adapts both models but optimises for a different outcome: enforceable equity claims rather than frictionless speculation. This introduces structural friction (4-8 weeks from deal to live market versus 30 seconds on Pump.fun), but that friction produces verifiable positions backed by real cap table entries.

The Virtuals Partnership

XMAQUINA partnered with Virtuals Protocol for the final community sale ahead of TGE, the first project launched under Virtuals’ Titan model. The auction sold out, raising $3.2M ($3.046M in USDC, 190.4K in $VIRTUAL) and allocating 92M $DEUS. The $VIRTUAL contributions seed a DEUS/VIRTUAL liquidity pool at TGE, with a committed TVL target of over $1M. The DAO separately allocated 18M $DEUS and $150K USDC toward liquidity through governance proposal XMQ-02. The partnership connects XMAQUINA to Virtuals’ user base of over 1M wallets and positions the project within one of the most active onchain ecosystems in crypto.

3.2 $DEUS

$DEUS is the coordination and value capture asset of the XMAQUINA ecosystem. It governs the DAO treasury, controls capital deployment, and determines how protocol cash flows are allocated. Maximum supply is fixed at 1B with no inflation. Full supply vests over 4 years.

Governance operates through a veToken model. Holders stake $DEUS to mint xDEUS for voting power. Voting weight increases with staking duration, starting at a base multiplier and scaling up to 12× after 12 months of continuous staking. A governance activation program allocates 1M $DEUS toward staking rewards, emitted linearly over 90 days from May 18, 2026. Governance operates through Aragon OSx, a modular framework that allows onchain proposal submission, treasury operations, and protocol parameter configuration.

xDEUS holders control treasury deployment, exit timing, and fee allocation. Following a liquidity event, governance may vote to distribute up to 40% of realised proceeds to active xDEUS holders, pro-rata based on multiplier-weighted balances. Where governance approves distribution, the remainder is retained in treasury for new allocations.

Value Accrual

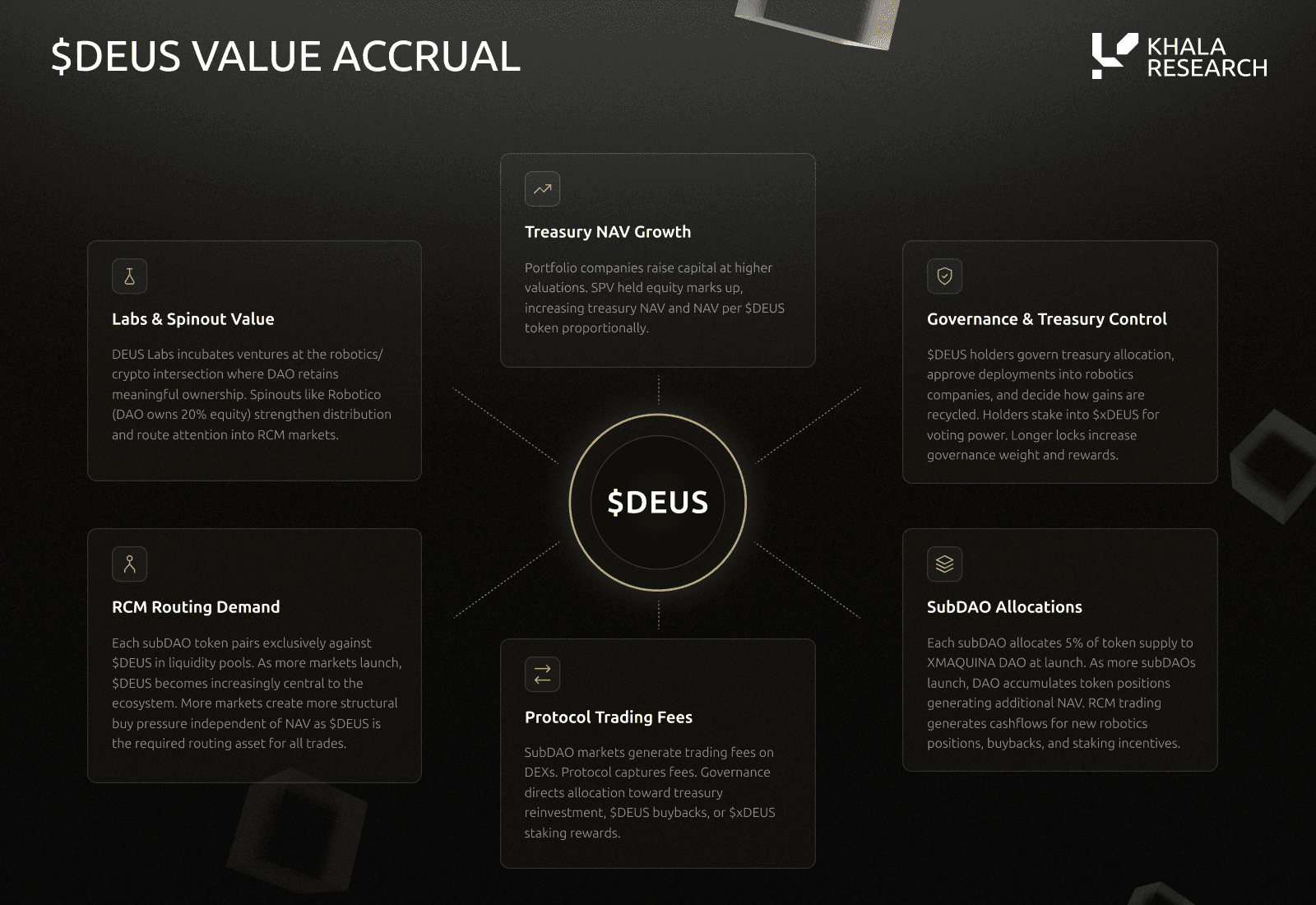

$DEUS captures value at six levels:

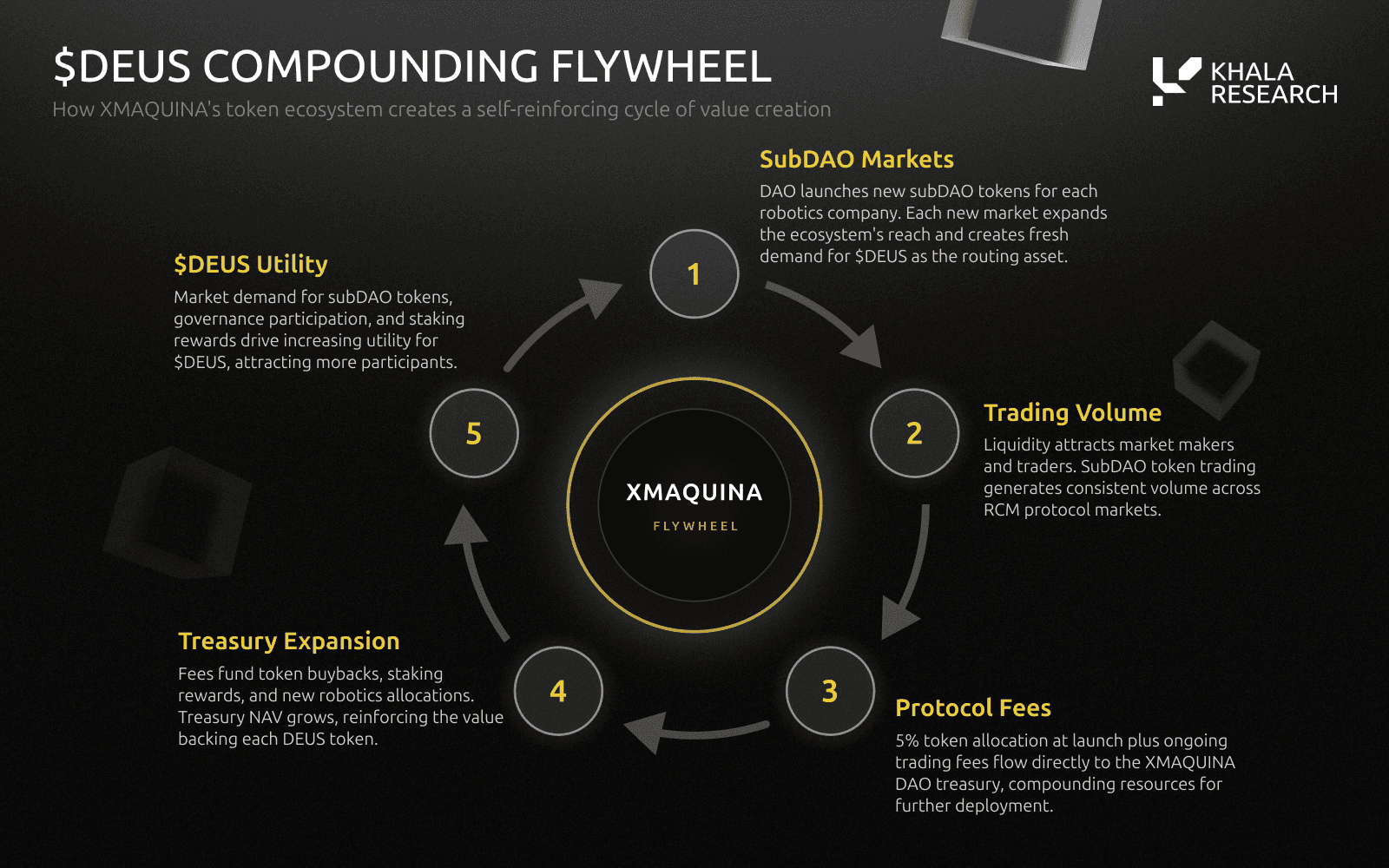

The first is protocol carry: every subDAO launched through RCM allocates 5% of its token supply to the DAO at launch. The DAO takes a position in every market it creates without deploying additional capital. At five active subDAO markets, the DAO holds 5% of five separate token supplies, each generating trading activity.

The second is routing demand. All subDAO tokens pair exclusively against $DEUS on DEX, making $DEUS the intermediary asset for every trade in every subDAO market. This follows the routing-asset model established by Bittensor, where $TAO pairs with all subnet tokens, and Virtuals Protocol, where $VIRTUAL denominates all agent markets. Both demonstrated that a base-pair token accrues structural demand proportional to the number of active markets and their volume.

The third is fee flow. Trading fees from subDAO DEX activity flow to the DAO treasury. Governance decides how to allocate them: new equity acquisitions, $DEUS buybacks, or xDEUS staking rewards. The allocation is not hardcoded. Token holders vote on deployment, which means the value accrual path adapts as the ecosystem matures.

The fourth is treasury NAV growth. The underlying portfolio appreciates independently of the token economy. When a portfolio company raises at a higher valuation, the DAO's mark increases. When a company IPOs or is acquired, the DAO realises gains. These returns compound alongside protocol-level revenue.

The fifth is DEUS Labs incubations. The DAO holds 20% of Robotico and will hold comparable stakes in future incubations. If spinouts reach product-market fit, the treasury marks appreciate at multiples that external portfolio entries cannot match, and each can become a new subDAO market on RCM.

The sixth is governance itself. $DEUS holders stake to mint xDEUS and control how all of the above is directed: which companies the treasury deploys into, how fees are allocated, when positions are exited, and whether proceeds go toward buybacks, staking rewards, or new allocations. Every mechanism above flows through governance.

The compounding case: fees from subDAO trading grow the treasury, a larger treasury funds more equity allocations, more allocations create more subDAO markets, more markets generate more fees.

NAV Premium Analysis

The DAO Portal reports a $28M treasury, but as noted in Section 3, $18M of this is the DAO’s own $DEUS tokens at the $0.06 Genesis price. The working figure, excluding self-valued $DEUS, is approximately $10M in robotics equity, cash, and tokens. Two frameworks apply. The treatment of treasury-held DEUS must be symmetrical in each.

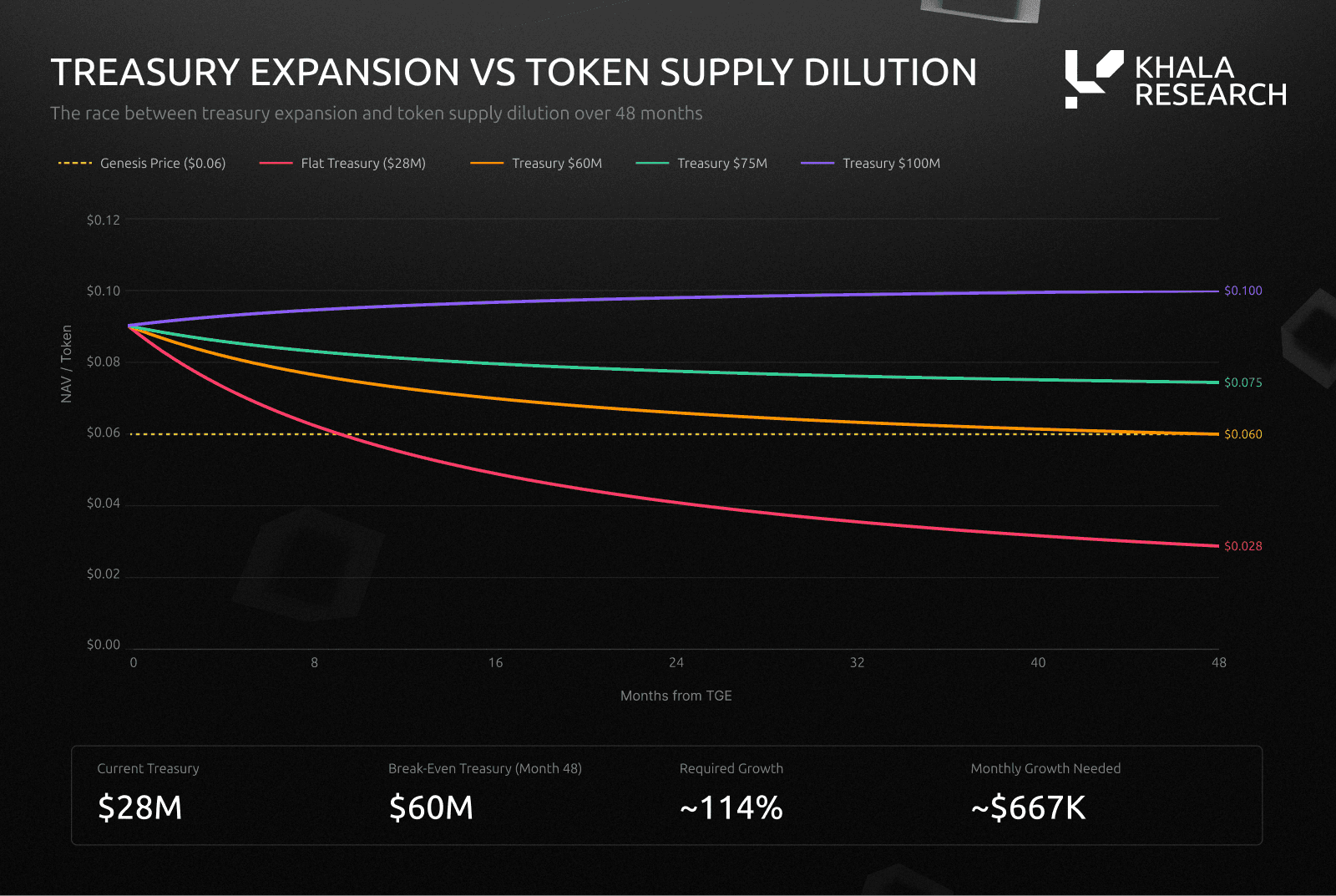

Method 1 includes treasury $DEUS in both FDV and NAV. The headline treasury is $28M ($6.7M robotics equity, $3.3M cash and stablecoins, 3.7M $PEAQ and 18M $DEUS). The full token supply is 1B. At a circulating supply of 314.7M tokens, the NAV per token is approximately $0.089. FDV at $0.06 is $60M. FDV divided by NAV equals $60M / $28M = 2.14x, or a 114% premium. This is internally consistent: the 300M $DEUS held in treasury counts as an asset and remains part of the supply base.

Method 2 removes treasury DEUS from both FDV and NAV. Treating treasury-held $DEUS as non-circulating, analogous to treasury shares, removes 300M tokens from both sides. Adjusted FDV is $42M (700M tokens at $0.06). Adjusted NAV is $10M (robotics equity, cash, crypto). Adjusted FDV divided by NAV equals $42M / $10M = 4.19x, or a 319% premium.

Comparing $60M FDV (full 1B supply) against $10M working NAV produces ~6x because it counts treasury $DEUS in the supply but refuses to count it as an asset. The opposite, comparing $42M adjusted FDV against $28M headline NAV, understates the premium at 1.5x. Which framework an allocator uses depends on whether they treat DAO-held $DEUS as a treasury asset or as non-circulating supply.

Working Treasury | Premium (at $0.06 $DEUS) |

|---|---|

$10M (current) | 4.19x |

$25M | 1.68x |

$42M | 1.0x |

A third lens is liquid-float market value to NAV. This is not the same as FDV / NAV. $DEUS has a fixed maximum supply of 1B, but the liquid float is smaller due to vesting, treasury reserves, and xDEUS staking. Under the vote-escrow model, staked $DEUS is non-transferable. A small liquid float can amplify premiums when demand exceeds immediately tradeable supply. This ratio is dynamic: as tokens vest, liquid supply increases. If the robotics portfolio appreciates and new treasury investments are added, NAV rises too.

Cross-checking against the live market: RoboStrategy (Section 3.1) trades at roughly 2.6-8.0x the most recently disclosed NAV. XMAQUINA's multiple sits below that under both methods (2.14x and 4.19x). There are some differences though. BOT is a passive portfolio with no redemption mechanism and no compounding revenue model. XMAQUINA adds active governance, protocol revenue potential via RCM, and incubation upside through DEUS Labs. It also adds execution risk, pre-TGE pricing uncertainty, and an untested protocol. Whether XMAQUINA can sustain a comparable premium depends on RCM volume materialising and the market pricing governance and ecosystem value alongside the underlying assets.

Over 48 months, the remaining 685.3M tokens vest, bringing the circulating supply to 1B. Under Method 1, the headline treasury divides across 1B tokens. A static $28M treasury means NAV per token drops to $0.028 at full dilution. The $0.06 price then requires the treasury to reach $60M by month 48, or approximately $667K in net monthly growth. RCM protocol fees, new equity allocations, portfolio appreciation, and eventual $DEUS market value all contribute. If RCM generates sustained volume, the compounding case is that fees grow the treasury, a larger treasury funds more equity allocations, and new allocations create more subDAO markets generating more fees.

The MicroStrategy Comparison and Its Limits

XMAQUINA’s documentation draws a parallel to MicroStrategy (now Strategy Incorporated), whose BTC premium has ranged from -30% to +200%, peaking at 3.89x mNAV on 20 November 2024 before compressing below 1x by late 2025 as competing treasury vehicles entered the market. The comparison has analytical value but overstates the similarity. MicroStrategy sustained its premium through equity issuance at premium prices to buy more BTC and $8.2B in convertible debt across six offerings at a weighted average coupon of 0.42%. The capital structure also carries escalating costs: annual preferred stock dividend obligations across STRK, STRF, STRD, and STRC had reached approximately $588M by August 2025 and continue to grow as new series are issued.

$DEUS can replicate one mechanism: if the market prices $DEUS at a premium, governance can deploy treasury $DEUS to acquire more robotics positions, growing NAV faster than dilution. It cannot replicate public Nasdaq liquidity ($DEUS is pre-TGE), real-time pricing (BTC trades 24/7; private robotics equity uses quarterly marks), or debt-market access. One structural difference works in XMAQUINA’s favour: the underlying robotics equity has defined exit paths (IPO, acquisition) that produce discrete value realisation events, unlike BTC which relies on perpetual appreciation.

CEF Discount Drivers

Most closed-end funds trade at persistent discounts to NAV, typically 9-14% for conventional vehicles. Scarcity-exposure funds can trade at extreme premiums, as RoboStrategy demonstrates. RCM addresses two of three structural drivers:

Driver | Why CEFs Discount | RCM Approach |

Management Fees | 2% AUM + 20% carry = 20%+ drag over 10 years | Protocol fees flow to treasury, not operators |

Illiquidity | 7 to 10 year lockups, no exit except haircut sales | subDAO tokens tradable 24/7 on DEX |

No Redemptions | Exit via secondary where spreads widen under stress | DEX provides exit. Governance can vote to liquidate. |

The redemption mechanism is partial: DEX exit depends on counterparty liquidity in subDAO token pools. Depth will develop alongside volume.

Governance Value: A Theoretical Framework

Note: this section applies a traditional fund economics lens to estimate what governance might be worth, not what $DEUS holders actually pay or receive. The DAO does not charge management fees. No one pays 2/20. This is an analytical exercise, not a description of actual cash flows.

$DEUS holders control treasury deployment, exit timing, and fee allocation. This governance right has economic value separate from the underlying assets. In traditional fund economics, the right to direct capital deployment is worth 2-4x annual management fees capitalised. Using the headline treasury ($28M), a conventional fund at 2% would generate $560K per year. Using the working treasury ex-DEUS (~$10M), that figure drops to $200K per year. Capitalised at 2-4x, governance value ranges from $400K to $800K (working) or $1.1M to $2.2M (headline), equivalent to $0.0013 to $0.007 per token at current circulating supply.

This represents 2-12% of the $0.06 Genesis price. The number is a reference point for thinking about how much of the token price is governance premium versus asset backing. It is not an actual fee stream and should not be treated as revenue. Its validity depends on governance being actively exercised (the current 6.7x average quorum suggests active participation), the treasury being managed competently, and RCM fees eventually materialising. If RCM protocol fees scale to $1M-$2M annually, governance value under this framework could represent 7-33% of the current price.

3.3 DEUS LABS

DEUS Labs is XMAQUINA’s in-house development studio, operating as an independent subDAO. Where the DAO treasury acquires minority positions in external companies at late-stage valuations, DEUS Labs builds net-new companies from inception with the DAO holding 20%+ equity. Robotico is the first incubation. The return profiles are different: external positions in companies like Figure AI or Apptronik offer exposure at established valuations, while incubated ventures offer pre-seed economics where a successful Series A could return 10-50x on deployed capital.

A second incubation (undisclosed) is scheduled for Q4 2026 per the roadmap. If DEUS Labs produces two to three viable companies over the next 24 months, the DAO’s ownership stakes could become the highest-returning positions in the treasury on a cost basis.

Robotico: Intelligence Layer for the Humanoid Economy

Robotico was approved through BOT-10 (83.9% approval, 3.29M votes). The DAO acquired 20% equity at $800K pre-money as the sole pre-seed investor, deploying $200K (3.1% of the robotics portfolio).

The platform aggregates and structures data on humanoid robotics companies for investors, researchers, and builders. Core features include a global humanoid directory covering 50+ companies, AI-powered signal monitoring (PR, research, funding, patents), VC investment tracking, an editorial platform with CMS and newsletters, and a creator publishing program with monetised expert profiles. The founding team comprises Ben Knaus (10+ years in Web3, AI, and data infrastructure; $160M+ in M&A) and Favio Velarde (former growth lead for Sologenic, Coreum, and SoloTex).

Robotico serves three functions within the XMAQUINA ecosystem: user acquisition (draws robotics-interested users toward the DAO), RCM distribution (links company profiles to subDAO token markets), and equity upside (DAO holds 20% of a company building sector-specific data infrastructure).

4. CATALYSTS & RISKS

Catalysts:

TGE and exchange listings. $DEUS transferability activates on TGE. Exchange listings follow. First live market pricing of $DEUS establishes whether the token trades above or below the $0.06 Genesis price and sets the baseline for all subsequent NAV analysis.

RCM Protocol launch (Q3 2026). The first subDAO markets go live. Early volume data in the first 30-60 days will signal whether the fee flywheel has traction. Even modest activity ($5M+ monthly) would validate the mechanism and generate the first protocol-level revenue for the treasury.

Portfolio company IPOs (2027 to 2028 window). Unitree is targeting a ~$7B IPO. Figure AI and Apptronik are on institutional radars for public listings in the same window. Any IPO or acquisition among the seven portfolio companies would crystallise gains and demonstrate the DAO's ability to capture pre-IPO returns for token holders.

New equity allocations. The Northstar Council has identified FieldAI, Skild AI, Physical Intelligence, Clone Robotics, RoboForce, AgiBot, Unitree, and Sunday Robotics as targets. The roadmap targets 10 treasury positions by Q3 2026. Each new allocation creates an additional subDAO market opportunity and broadens portfolio diversification.

RCM expansion phase (Q4 2026). Perpetuals, prediction markets, and additional subDAO listings are on the roadmap. If the initial subDAO markets gain traction, the expansion phase introduces new trading primitives that could multiply protocol fee generation.

Second DEUS Labs incubation (Q4 2026). An undisclosed second incubation is scheduled per the roadmap. A second 20%+ equity position at pre-seed terms would double the incubation portfolio and test whether the DEUS Labs model is repeatable.

Risks:

Regulatory Risk. subDAO tokens are structured without equity rights, but regulatory classification remains uncertain. XMAQUINA obtained legal opinions from three firms classifying $DEUS as a utility token outside Howey. The opinions cover five jurisdictions. Whether they hold under enforcement is untested. The RCM protocol plans a Reg S framework with KYC/KYB, but subDAO token classification has no precedent. The SEC/CFTC March 2026 interpretation maintains investment contract analysis applies regardless of token label.

Counterparty and Custodial Risk. Andersen LLP attested six treasury allocations. The remaining two positions and future allocations have no independent verification schedule. SPVs operate through regulated broker-dealers with SIPC coverage to $500K per account, but no platform insures against investment loss or company failure.

Treasury Concentration and Self-Valuation. Headline treasury of $28M includes $18M in self-valued $DEUS at the $0.06 Genesis auction pricing because $DEUS has not yet traded on any market. Working treasury is approximately $10M. The robotics portfolio concentrates 84.0% in three positions, all pre-revenue, marked at last-round pricing and dependent on 2026-2028 commercialisation timelines. Common shares in Figure AI and 1X are subordinate to preferred holders.

Down-Round Risk. All portfolio positions are pre-revenue or early-revenue, marked at last-round pricing. If any portfolio company raises a down round, the DAO’s mark compresses and Treasury NAV declines. Common share positions (Figure AI, 1X) are subordinate to preferred holders in a liquidation or restructuring.

Routing Asset Risk. Fragmenting $DEUS liquidity across multiple subDAO token pairs creates slippage that could undermine usability at size. Users may route through stablecoins instead, reducing $DEUS to a ceremonial base pair with limited actual routing function. This risk resolves only if liquidity depth develops across subDAO markets.

Key Person Risk. Deal sourcing depends on the core team's broker relationships. Three co-founders share responsibilities, a Scoring Committee of embedded advisors conducts due diligence and shares the broker network, and platform relationships through Forge Global, Zanbato, Hiive, and EquityZen are institutional rather than personal. These layers reduce but do not eliminate risk. No formal succession plan has been disclosed.

Vesting Dilution. 685.3M tokens vest over 48 months. If treasury growth does not outpace dilution, NAV per token compresses from $0.089 (circulating) to $0.028 (fully diluted). 33% of the DAO Treasury allocation (99M $DEUS) unlocks at TGE and is deployable via governance vote, adding to potential TGE sell pressure.

5. CLOSING THESIS

XMAQUINA has placed a DAO's capital onto the cap tables of seven private humanoid robotics companies. The positions are documented, the treasury is transparent, and at least two have appreciated materially from entry. The 1X allocation is up 119%. The Apptronik preferred position has doubled. The total treasury stands at $28M across equity, crypto, and cash, governed by a token holder base that has passed 14 proposals at an average of 6.7x quorum.

The harder question is whether the model scales. The RCM Protocol is the mechanism that converts XMAQUINA from a small DAO investment vehicle into something with compounding economics. Without it, $DEUS is a governance claim on a working treasury of approximately $10M in equity and cash. With RCM generating volume, $DEUS captures protocol fees, structural demand from subDAO pairings, and governance rights over an expanding pool of assets. The difference between those two outcomes is the entire investment case.

What makes XMAQUINA worth watching is the sector it occupies and the timing of its attempt. Humanoid robotics funding hit $14B in 2025. IPOs are anticipated in the 2027 to 2028 window. The capital being deployed into private robotics far outstrips the mechanisms available for broader participation. XMAQUINA is not the only project that will try to fill it, but as of today, it is the one with equity on the cap tables, a governance system that functions, and a protocol roadmap with community backing.

The premium at $0.06 buys one thing: a bet that RCM volume materialises or positions appreciate before vesting catches up. Everything else in the report is context for that.

This framework is illustrative and does not constitute investment advice. Allocations should reflect individual risk tolerance.

Scenario | Timeline | Conditions | Ecosystem Implication | Monthly Signal |

|---|---|---|---|---|

Bear | 2027 | RCM fails to launch or generates negligible volume. Portfolio companies delay commercialisation beyond 2028. $DEUS trades below $0.06, compressing headline treasury. Regulatory action restricts subDAO trading. | $DEUS trades at or below fully diluted NAV. Treasury shrinks. Governance participation falls below quorum. | RCM monthly volume <$1M. Quorum <100%. |

Base | 2027 | RCM launches with 2-3 subDAO markets. Moderate volume. One portfolio company raises at higher valuation. Treasury grows through fees and new allocations. | $DEUS at moderate premium to fully diluted NAV. Portfolio expands toward 10 allocations. | RCM monthly volume $5M to $20M. 1+ new subDAO auction. |

Bull | 2027 | RCM becomes primary venue for onchain robotics exposure. Multiple active markets. Portfolio company IPO crystallises gains. $DEUS trades at sustained premium. | $DEUS at sustained premium. XMAQUINA establishes category. | RCM monthly volume >$25M. 3+ active subDAO markets. |

DISCLAIMER

This report was commissioned by XMAQUINA. Khala Research received compensation for its production. All analysis, conclusions, and risk assessments are independently formulated by Khala Research. This report does not constitute investment advice, a solicitation to buy or sell any asset, or a recommendation of any kind. The $DEUS token has not yet launched. Readers should conduct their own due diligence and consult legal and financial advisors before making any investment decisions.

APPENDIX

$DEUS TOKENOMICS

Category | Allocation | Vesting |

Genesis Auctions | 23.2% | 33% at TGE, 67% linear over 12 months |

DAO Treasury | 30.0% | 33% at TGE (99M DEUS, deployable only via governance vote), 67% linear over 48 months |

Liquidity & Ecosystem | 8.3% | 100% at TGE. Includes unallocated Genesis supply per XMQ-02. |

Strategic Contributors | 8.0% | 7.5% at TGE, 6-month lock, 18-month linear vest. |

Core Contributors | 12.5% | 12-month lock, then 12-month linear vest. |

Foundation | 7.5% | 7.5% at TGE, 12-month lock, then 12-month linear vest. |

DEUS Development Lab | 7.5% | 33% at TGE, 67% linear over 24 months. |

RCM Protocol | 2.0% | 100% at TGE. Development and legal structuring. |

Advisors | 1.0% | 12-month lock, then 12-month linear vest. |

Source: XMAQUINA documentation, May 2026.

Max supply: 1B (fixed, no inflation). Circulating at TGE: ~31.5% including 9.9% in DAO Treasury (governance-locked). ERC-20, omnichain-compatible. Governance: veToken (xDEUS).

Note: 33% of the 300M DAO Treasury allocation (99M DEUS) unlocks at TGE and could theoretically be deployed or sold by governance vote, contributing to initial supply pressure.