BITTENSOR: THE INVESTMENT HISTORY

Bittensor has become the most active capital market ecosystem for crypto-enabled AI startups. The Khala Research team takes you back from the TGE of TAO, with a single token, to today with 128 subnets and a pending spot ETF, to track how investing in Bittensor has shifted.

KEY TAKEAWAYS

AI infrastructure is the defining equity narrative of this generation, and Bittensor is the most developed open alternative in production. AI infrastructure stocks outperformed every major index in 2025, while model development consolidated behind three closed labs controlling access to the most capable models and the most valuable training data. Bittensor launched in January 2021 as an open-source alternative to closed-lab AI infrastructure and is now the most active public market for open-source AI intelligence.

dTAO replaced validator discretion with market-determined emissions, unlocking an entrepreneurial AI capital market. Before the upgrade, 64 validators (with documented conflicts) controlled 7,200 TAO in daily emissions, routinely allocating to subnets they operated or held personally. dTAO gave every subnet its own liquidity pool and alpha token, growing the subnet aggregate market cap from $4M at launch to a peak of $1.47B in March 2026. Emissions now flow to subnets with traction, not validator relationships.

External revenue is now surfacing from subnets that do not depend solely on emissions. SCORE holds enterprise contracts with PwC France, AVIA across 3,000 petrol stations in 15 countries, and Reading FC. Targon operates a confidential GPU marketplace and powers external AI workloads including Venice AI and Dippy AI. Vanta returned $48K net in its first profitable month from external trading activity.

Grayscale moved from trust launch to S-1 filing in 18 months (vs. BTC's 10 year long journey): The GTAO trust began OTC trading in December 2025 and filed for spot conversion by year-end. Spot Bitcoin ETFs have onboarded over $60B in cumulative net inflows, with the first year delivering $36.6B.

INTRODUCTION

Frontier AI development has concentrated rapidly into a small number of closed labs. Compute, data, and increasingly model weights sit behind access controls and commercial APIs. The fight today is less about which models are most capable and more about whether the infrastructure underpinning artificial intelligence will be accessible to the public.

Anthropic, OpenAI, and Google DeepMind are entities creating and gating access to the most powerful models, accumulating the most training data, and setting the terms on which the rest of the world interacts with AI. That outcome is the default consequence of building on infrastructure controlled by commercially motivated parties.

A generation of crypto-native AI entrepreneurs have chosen a different path, using crypto rails to coordinate global capital and talent in support of open source AI. Bittensor is the most developed expression of that bet. The founding team bootstrapped the protocol from 2019 through 2021 the same way miners earn TAO today: through work, not fundraising. Every TAO was mined from genesis, and the founding team earned their tokens the same way everyone else did. There was no pre-mine, no team allocation, and no venture capital. Every TAO from genesis was earned through network participation. We first covered it in February 2026, and it remains one of the only structural counters to the closed-source labs available in any public market today, crypto or equity.

For allocators who believe open AI infrastructure will compound at scale, Bittensor combines a live market for AI intelligence with a base-layer token, a growing suite of institutional access products, and an open architecture that anyone can build on without permission.

Since its token generation event in 2021, Bittensor has evolved into one of the most active capital markets for crypto-enabled AI companies in the world. TAO opened at ~$91 on its first exchange listing in early 2023, peaked above $750 in March 2024, and trades near $210 as of June 2026. TAO carries a $2B market cap, ~2.4x the aggregate value of all 128 subnets combined. This report profiles three investment eras of the protocol: from genesis mainnet in 2021 through to the institutionalisation of the most important open-source infrastructure project in production today.

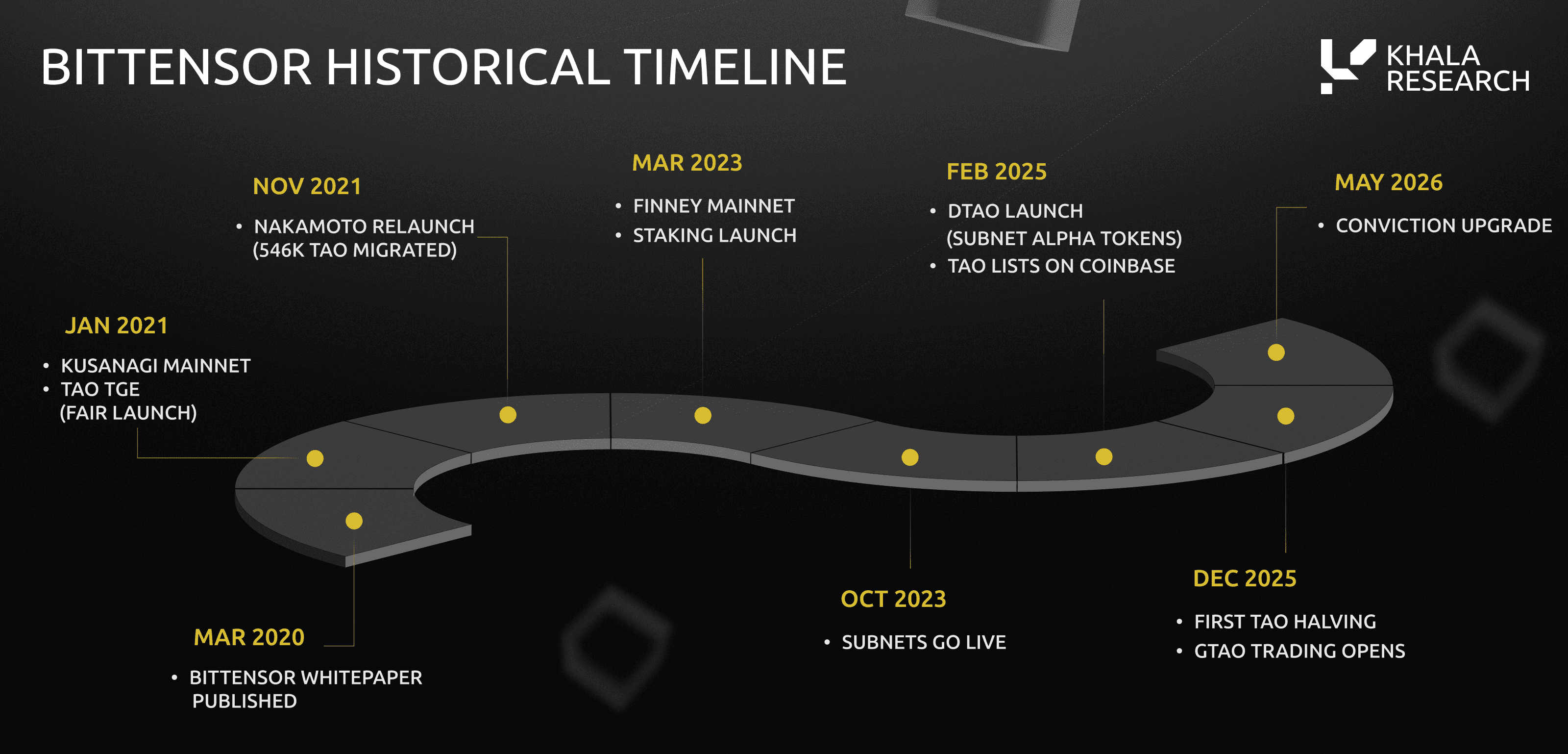

March 2020: The Bittensor whitepaper introduced a decentralised market where machine intelligence is priced by peer systems. It established the theoretical foundation for the protocol's incentive mechanism.

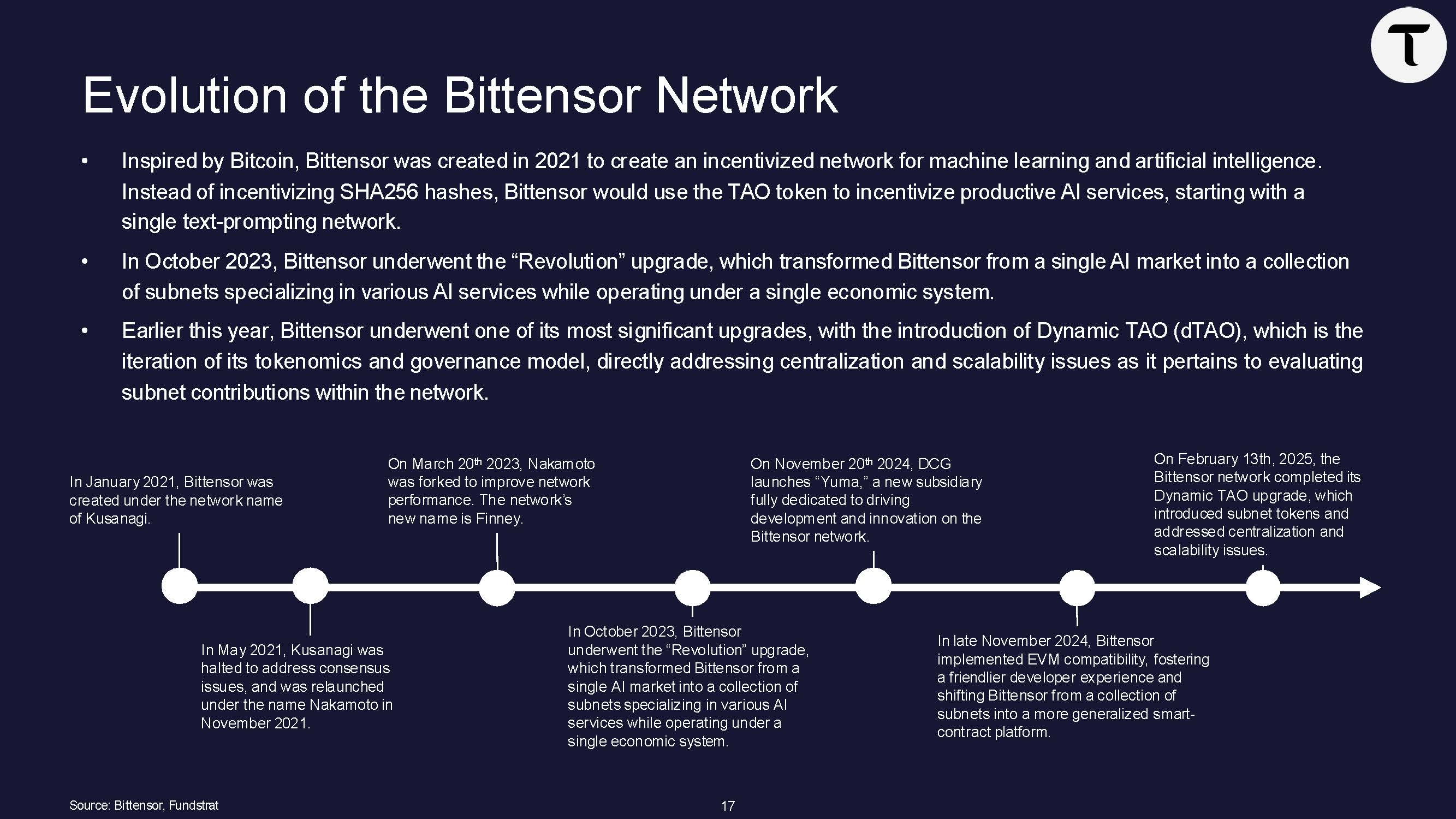

January 2021: The Opentensor Foundation launched Kusanagi with no pre-mined tokens and no allocations to insiders. Every TAO from genesis was earned through mining.

November 2021: The network relaunched as Nakamoto from block 0 after Kusanagi paused in May. All 546,113 previously mined TAO migrated to the new proof-of-stake chain.

March 2023: Nakamoto forked to Finney, introducing subnets and delegated staking on mainnet. Finney resolved kernel-level performance issues and remains the live iteration of Subtensor.

October 2023: The subnet framework activated on Finney mainnet. Each subnet operates as an independent task-specific market where miners compete on outputs and validators score results.

February 2025: Dynamic TAO deployed to mainnet, replacing manual validator voting with AMM pool prices as the emission mechanism. Coinbase listed TAO seven days later on February 20.

December 2025: The first TAO halving executed at block 7,103,976, cutting daily issuance from 7,200 to 3,600 TAO. The Grayscale Bittensor Trust (GTAO) began trading on the OTCQX Best Market on December 11.

May 2026: The Conviction Upgrade deployed following Covenant AI's sudden exit. All subnet owner emissions are now auto-locked on arrival; exits require a public onchain unlock transaction with a timed release schedule.

ERA 1: GENESIS (2021-2023)

Bittensor mainnet launched on January 3, 2021, publicly known as Kusanagi, with a token design that required miners to submit machine learning output for validator scoring. Meet the threshold, earn TAO. Miss it, earn nothing. Every TAO from genesis was earned through network participation.

Source: Grayscale’s Bittensor Report, April 2025

The founding team mined TAO through the same mechanism as everyone else. Every token they sold had been earned on the network, not allocated at genesis. Between 2021 and 2023 they sold roughly 600,000 mined TAO through private OTC transactions to Firstmark, DCG, and Polychain at approximately $18 per token, raising $10.8M in early development funding. No public market existed until the first exchange listings.

Four months after launch Kusanagi encountered a consensus failure. The network could not agree on block validity under the load of coordinating distributed miners and validators. Block production stopped in May 2021. Rather than patch a broken system, the team rebuilt from block zero, migrating 546,113 previously mined TAO to a new chain called Nakamoto that November. No user funds were affected.

Nakamoto ran through 2022 and into 2023. In March 2023 the network forked to Finney. The subnet framework activated in October 2023, expanding beyond text generation into image, storage, and pre-training. By then the first subnets were built around open inference and compute tasks: produce output, have it scored by validators, earn TAO if the score was high enough. The models were smaller and the benchmarks less sophisticated than what exists today, but the mechanism was the same.

Some of the early subnets:

SN | NAME | PURPOSE |

|---|---|---|

SN0 | Root | The network backbone that determined emission distribution per block to each subnet. Root also served as the Senate, where the top 12 staked validators held veto power on protocol proposals. |

SN1 | Text Prompting | The original Opentensor Foundation subnet. Miners produced LLM completions that validators queried, judged, and ranked. It proved the incentive layer could coordinate inference work at scale. |

SN2 | Machine Translation | One of the first three user-created subnets registered in the opening week. Miners translated text across languages through machine learning models. |

SN3 | Multi-Modality | This subnet extended the prompting template across text, image, and audio, enabling systems to process and generate information beyond plain text. |

SN4 | Image Generation | Miners produced images from text prompts. Validators scored output quality. It was the first proof that the incentive layer could coordinate generative work as well as inference. |

Early slots beyond these ran variations on the same inference template. The network was proving that decentralised task markets could produce real outputs and attract real participants. TAO’s first exchange listings in March 2023 opened at ~$91 before dropping to ~$30 that May. The market had seen proof of coordination. The drop showed the market wanted proof of demand.

By March 2024 TAO reached $757, ~25x from the low. The token's price reflected subnet growth but emission allocation reflected validator relationships. Emission weights were publicly visible onchain, but visibility and fairness are different things. The daily emission of 7,200 TAO distributed across the network was controlled by the top 64 validators by stake, a small cohort with known conflicts of interest. Validators routinely assigned heavier weights to subnets they operated or were personally invested in. Growing a subnet's share meant convincing that cohort, not demonstrating product traction. The mechanism that was supposed to reward intelligence was being gamed by political proximity. Validator relationships outweighed product quality in emission allocation. A good subnet with weak validator ties went hungry. A bad subnet with the right validator connections ate anyway.

The proposal that would change this was already being written by someone who saw good subnets go hungry...

ERA 2: DTAO (2023-2025)

2024 changed what institutional capital could do in crypto. The BTC spot ETF launched in January and onboarded over $60B in cumulative net inflows by late 2025, driving Bitcoin to a new all-time high. Stablecoins reached $310B in circulation by the end of 2025, up 131% from $134B in January 2024. Traditional finance now treated onchain capital formation as an asset class. Bittensor operated through all of it as a mined token with no publicly available regulated vehicles, no custodial products, and no institutional pipeline.

The network was tested before it could join that capital. In July 2024, a compromised PyPI package drained approximately 32,000 TAO (~$8M) from operator wallets. The attackers distributed malicious code disguised as a legitimate Bittensor package. Once imported, the code monitored for wallet operations requiring coldkey access and exfiltrated decrypted private keys to a remote server. The Opentensor Foundation halted the blockchain in safe mode, audited the codebase, and removed the malicious package. TAO dropped 15% before recovering within days. Consensus held. The blockchain itself was never compromised. The exploit reached through developer tooling, not the protocol layer.

That was a security test. The deeper problem was structural and had been festering since before the exploit. Validators had been assigning heavier emission weights to subnets they operated or were personally invested in, replacing merit with proximity. On January 9 2024 Jacob Steeves published BIT001: Dynamic TAO, the formal proposal to replace validator committee allocation with market-driven emissions.

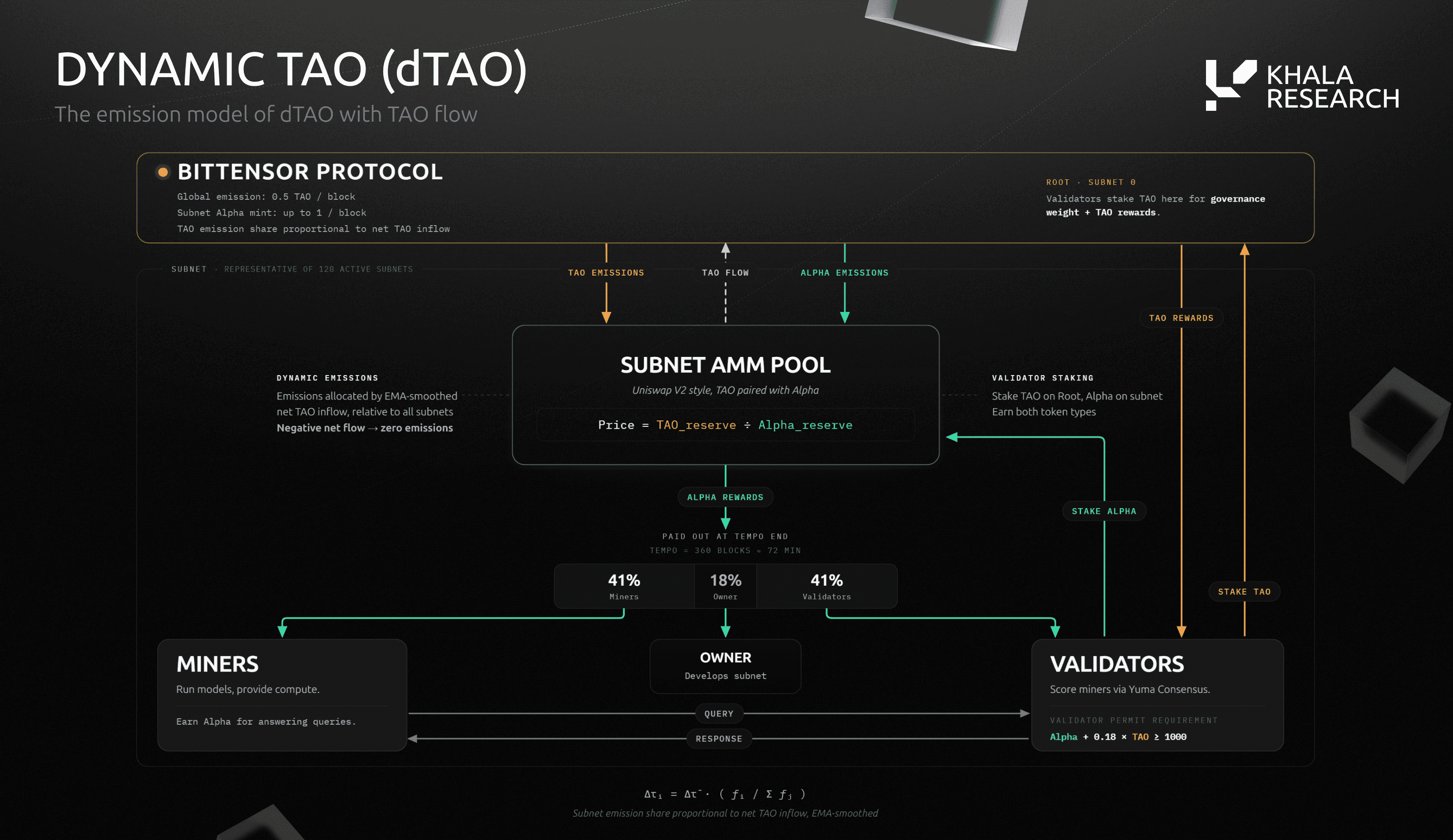

The upgrade would give every subnet its own AMM liquidity pool and alpha token. A holder staking TAO into a subnet swapped it for that subnet's alpha. Emissions would flow to subnets proportionally to the market demand for their alpha token, not by validator committee vote. Each subnet would become a liquid, independently priced asset. A subnet operator with product traction could attract capital directly. A subnet without it would see its alpha token price the lack of demand.

The mechanics, as specified in BIT001, were straightforward:

Every subnet gets its own automated market maker paired with a subnet-specific alpha token.

When a TAO holder stakes into a subnet, they are executing a swap: TAO enters the subnet's liquidity pool and receives that subnet's alpha token. Emissions flow to subnets proportionally to the market-driven demand for their alpha token.

Every subnet becomes a liquid, independently priced asset. The market signal that had been unable to reach the emission system under the root network could now reach it directly.

No single person can change the Bittensor protocol. The Triumvirate (three foundation leaders) drafts upgrades. The Senate (12 delegates elected by major stakeholders) votes on them. Both approved dTAO in February 2025 and the upgrade went live on February 13.

Jacob Steeves and Ala Shaabana co-founded Bittensor in 2019 with the thesis that machine intelligence markets should be open and meritocratic. The root network's validator cohort was the antithesis of that. Steeves, a former Google software engineer and mathematics and computer science graduate from Simon Fraser University, had been mining TAO alongside the network's participants since genesis. Shaabana, a former Assistant Professor at the University of Toronto and postdoctoral researcher at the University of Waterloo, had spent years watching validator discretion distort the emission system he had helped design, rewarding relationships over product quality. The Triumvirate and Senate approval of the BIT001 proposal in February 2025 restored that principle through onchain governance. The full technical specification is available on GitHub, later formalised in the dTAO whitepaper.

After the upgrade, each subnet had its own AMM pool, its own alpha token, and its own market-determined issuance rate. Root validator consensus was now replaced by a price mechanism. Alpha tokens traded against TAO in their own liquidity pools, giving every subnet a live market price, anchored to TAO. Emissions flowed by demand, not discretion. By the time dTAO activated, TAO had corrected from its March 2024 peak to ~$430.

Source: Crucible Labs Bittensor Report, Jan 2025

As of April 2025 the network had 82 deployed subnets, which grew to the maximum cap of 128 by September 2025, creating a vibrant ecosystem of investable companies within a year. The subnet alpha market started at $4M and reached $500M within ten weeks.

The hard cap of 128 subnets is enforced by an automatic pruning mechanism: when a new subnet registers and all slots are full, the protocol removes the subnet with the lowest exponentially weighted moving average price, provided it is outside its four-month immunity period. This gives new entrants time to establish themselves while preventing inactive subnets from drawing emissions indefinitely.

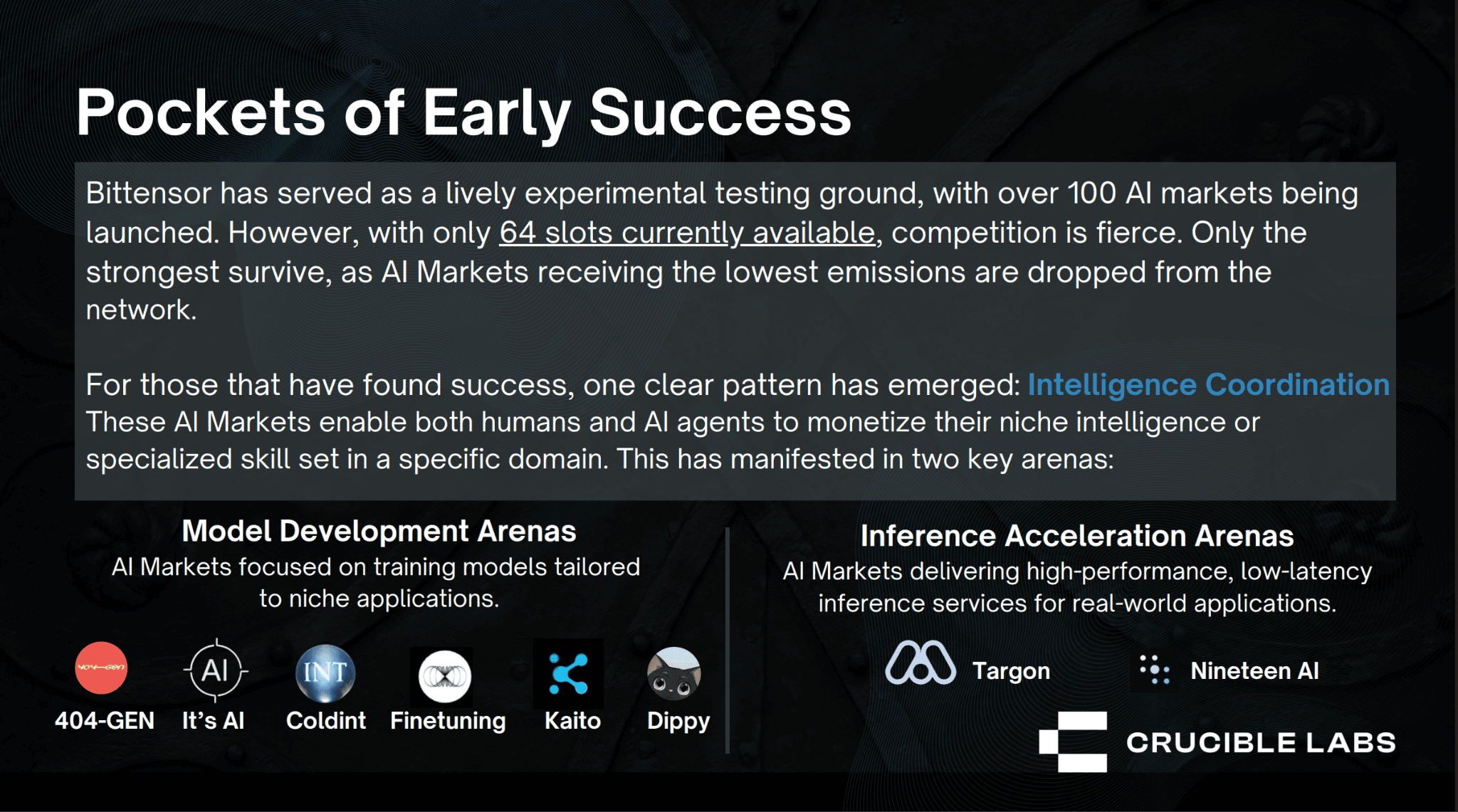

Bittensor's 128 subnets cover verticals including inference, compute, data scraping, sports AI, drug discovery, trading signals, agentic AI and more. A holder who believed a specific subnet was undervalued could express that view directly, and a subnet operator building a real product could attract capital based on commercial traction rather than validator relationships.

The current three largest by market cap are Chutes (SN64) at ~$76M, a decentralised compute and inference network; Targon (SN4) at ~$59M, a confidential GPU marketplace for AI training; and lium (SN51) at ~$50M, a decentralised GPU rental marketplace.

The Khala team has taken notice of four subnets with accelerating external revenue or signed enterprise contracts, illustrating what dTAO has done to the ecosystem:

SCORE (SN44) converts live video into structured enterprise data pipelines without proprietary camera hardware. Signed customers include Reading FC, AVIA (3,000 petrol stations across 15 European countries), and Lavance (7,000 vehicle wash stations). PwC France announced a strategic alliance in April 2026 to embed Manako's Business Operations World Model into advisory services across retail, logistics, energy, and public infrastructure. The subnet won Paris Blockchain Week's Start In Block 2026, beating more than 1,000 startups at the Louvre.

MetaNova (SN68) built a drug discovery subnet targeting psychiatric indications. 11M molecules have been screened against biological targets, with the combinatorial library expanding to 65B compounds. The subnet partnered with OnePot, a robotics-driven synthesis lab that raised $13M from Fifty Years and Khosla Ventures, with angel support from OpenAI co-founder Wojciech Zaremba and Google Chief Scientist Jeff Dean. OnePot's platform compresses typical synthesis timelines from months to days.

Vanta (SN8) built a decentralised prop trading network with funded accounts for traders competing across forex, crypto, and equities. Miners submit directional signals evaluated on risk-adjusted returns by onchain validators. In March 2026, Vanta reported $100K in monthly alpha fees collected against $52K in miner emissions, $48K net. The team is also building Hyperscaled, a decentralised prop firm infrastructure combining Bittensor and Hyperliquid.

Targon (SN4) operates a confidential GPU marketplace with hardware-level Trusted Execution Environments that keep models encrypted even from the infrastructure provider. Venice AI trained its Uncensored 1.2 model on the subnet’s GPUs and Dippy AI, a consumer platform with 8.6M users, routes roughly half of its text inference through Targon. The subnet generates $10.4M in ARR. Manifold Labs raised $10.5M in Series A alongside Ram Shriram, Tobi Lutke, and the Bittensor co-founders.

The common thread across these four is that each has an external customer or demonstrable market demand signal that is independent of the emission mechanism. This is what dTAO made visible. The subnets that can attract staking based on real demand are distinguishable from those that cannot.

Source: Learn Bittensor

Critical to the network's growth is the miner base, the supply side that makes every subnet operational. A miner pays a TAO burn to register on a specific subnet, receives a UID, and runs hardware suited to that subnet's task. Validators send requests, score the outputs, and rank miners against each other. Top performers earn that subnet's alpha token. Poor performers get pruned when the subnet fills and their immunity period expires. There is no tenure and no guaranteed slot. Performance determines survival, not seniority. The meritocracy the founders wrote into the protocol at genesis applies to every miner. From near-zero at genesis in 2021, growth accelerated with each new subnet launch. Every new slot created a fresh emission stream to compete for, drawing in miners whose hardware or model specialisation suited that subnet's task. As of June 2026, 2,300 miners hold UIDs across the network, with hardware spread across North America, Europe, and East Asia. Some run continuously. Some rotate between subnets as demand and specialisation shift.

The market was no longer an experiment by late 2025. It had the depth, products, and revenue to attract the institutional capital that was already assembling at the edges.

ERA 3: INSTITUTIONAL ERA (2025+)

By late 2025 the protocol had become a structurally different asset from the one that launched in 2021. The first halving occurred in December 2025, cutting daily emissions from 7,200 TAO to 3,600 TAO on a Bitcoin-style schedule with a 21M hard cap.

Institutional capital arrived in two waves. The first came through the BTC spot ETF, which helped legitimise onchain assets for traditional allocators. The second wave came from AI infrastructure stocks, which outperformed every major index in 2025 and established AI as the dominant equity narrative and, by extension, created a favourable environment for any protocol positioned as the compute layer for machine intelligence. The same allocators who backed both trades started looking for the coordination layer that would run machine intelligence at scale. Bittensor was the only onchain protocol built for that job.

Grayscale launched the first regulated TAO vehicle in June 2024. By late 2025, institutional capital had found its way into Bittensor through trusts, native asset managers, and non-custodial indexes. The infrastructure miners built from near-zero in 2021 was now accessible to allocators who filed SEC disclosures and ran compliance checks. That was a different world from 2023, when TAO first started trading on exchanges. By March 2026, the combined market cap of all subnet tokens peaked at ~$1.47B.

In April 2026, Covenant AI, operator of Templar, Basilica, and Grail, publicly departed Bittensor. The founder accused Jacob Steeves of centralised control and liquidated approximately 37,000 TAO (~$10M), triggering an 18-27% price drop and over $9M in long liquidations. The network itself never paused. Blocks continued, subnets produced work, and emissions flowed on schedule. The governance debate that followed was messy, but it happened in public channels.

3.1 STRUCTURED CAPITAL

Six vehicles arrived with six different answers to the same question: how should an allocator own Bittensor? Grayscale built a brokerage ticker. Yuma built a subnet picker. Stillcore built a reserve-asset fund. Unsupervised built a TAO accumulator. TrustedStake built an index that removes the manager entirely. None of them existed before 2024.

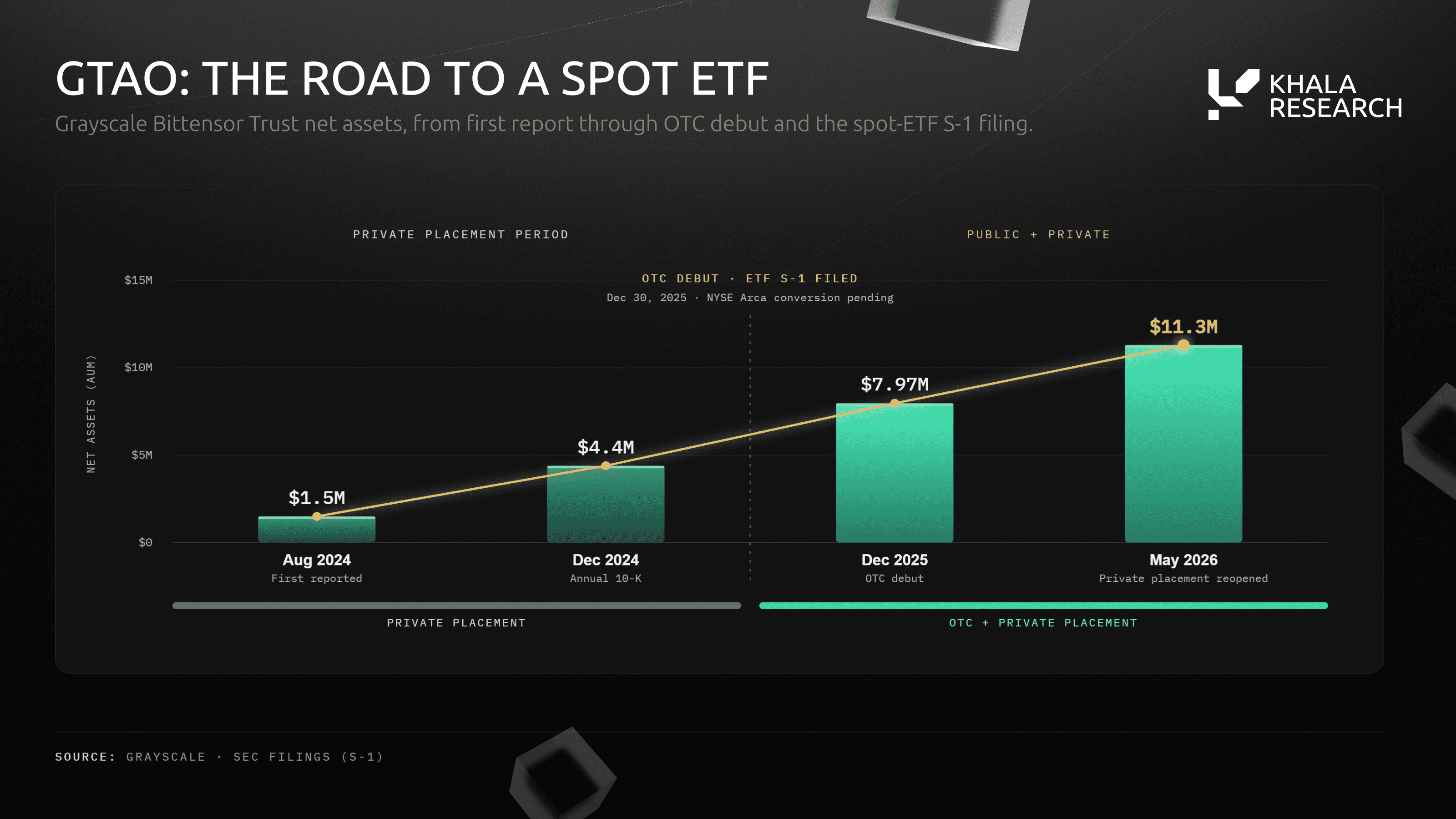

DCG has built two vehicles for Bittensor exposure. The first is the Grayscale Bittensor Trust (GTAO), which holds $11.7M in AUM as of March 31, 2026 per its quarterly SEC filing. It trades at a 59.9% premium to NAV, the kind of structural demand signal that typically indicates a product with no close substitute. The trust began as a private placement in June 2024, moved to OTC Markets that December as an SEC-reporting entity, and filed an S-1 for ETF conversion by year end. Bitcoin took over a decade to get a spot ETF. GBTC held $28B in AUM at conversion. Grayscale launched the GTAO trust and filed an S-1 in eighteen months. Approval remains pending.

DCG's second vehicle is Yuma, a Bittensor development studio and accelerator. In October 2025, DCG anchored Yuma's asset management division with $10M, making it the largest direct allocation to a Bittensor-native fund at that point. The fund runs two strategies denominated in TAO, both requiring accredited investor status. We explored Yuma's subnet thesis in detail on the Supercycle Podcast.

Evan Malanga, Chief Revenue Officer of Yuma, on the Supercycle Podcast.

The Safello Bittensor Staked TAO ETP (STAO) listed on SIX Swiss Exchange in November 2025 and cross-listed to Nasdaq Stockholm and Euronext Paris by June 2026. It holds ~$3M in AUM and is backed by staked TAO, with yield accumulated daily in NAV and reinvested automatically. Grayscale's GTAO S-1 explicitly prohibits staking. That distinction matters for allocators who want exposure plus yield.

Stillcore Capital launched in September 2025 with a "Third Great Ecosystem" framing that positions Bittensor alongside Bitcoin and Ethereum. Founded by Mark Jeffrey and Rob Greer, the fund lists Jason Calacanis as a consulting partner and describes Bittensor as "Bitcoin of AI" in its fund materials. Calacanis predicted a 200x TAO rally from a $2.5B market cap on an episode of This Week In Startups in March 2026. The fund runs three pillars: TAO as a reserve asset plus yield, concentrated positions in the top 5-10 subnets by market cap, and direct support for new subnet creation.

Unsupervised Capital, launched in April 2025 and anchored by Crucible Labs, is a TAO-denominated liquid token fund. Managing partner Sami Kassab, formerly of Messari and OSS Capital, has published an original analysis of compute subnet ARR and a high-margin subnet investment thesis. The fund's single objective is to accumulate more TAO for LPs than passive staking or simple indexing would generate.

TrustedStake, founded in 2024 by Douglas Albert and Alex Kiriakides, offers non-custodial index exposure across 40+ subnets. As of June 2026, the live dashboard shows $4.7M in AUM across 2,232 nominators. While every other vehicle asks allocators to trust a fund manager, TrustedStake answers a different question: what if the allocator does not want to pick a fund at all?

As of June 2026, verifiable institutional vehicles for Bittensor span Grayscale's GTAO Trust ($9.4M), the Safello STAO ETP ($3M) and TrustedStake ($4.7M). Yuma Asset Management, Stillcore Capital and Unsupervised Capital are active but do not disclose AUM.

The disclosed total is small against a $2B market cap. But these vehicles are the first regulated or semi-regulated pathways for allocators who cannot or choose not to hold spot TAO directly.

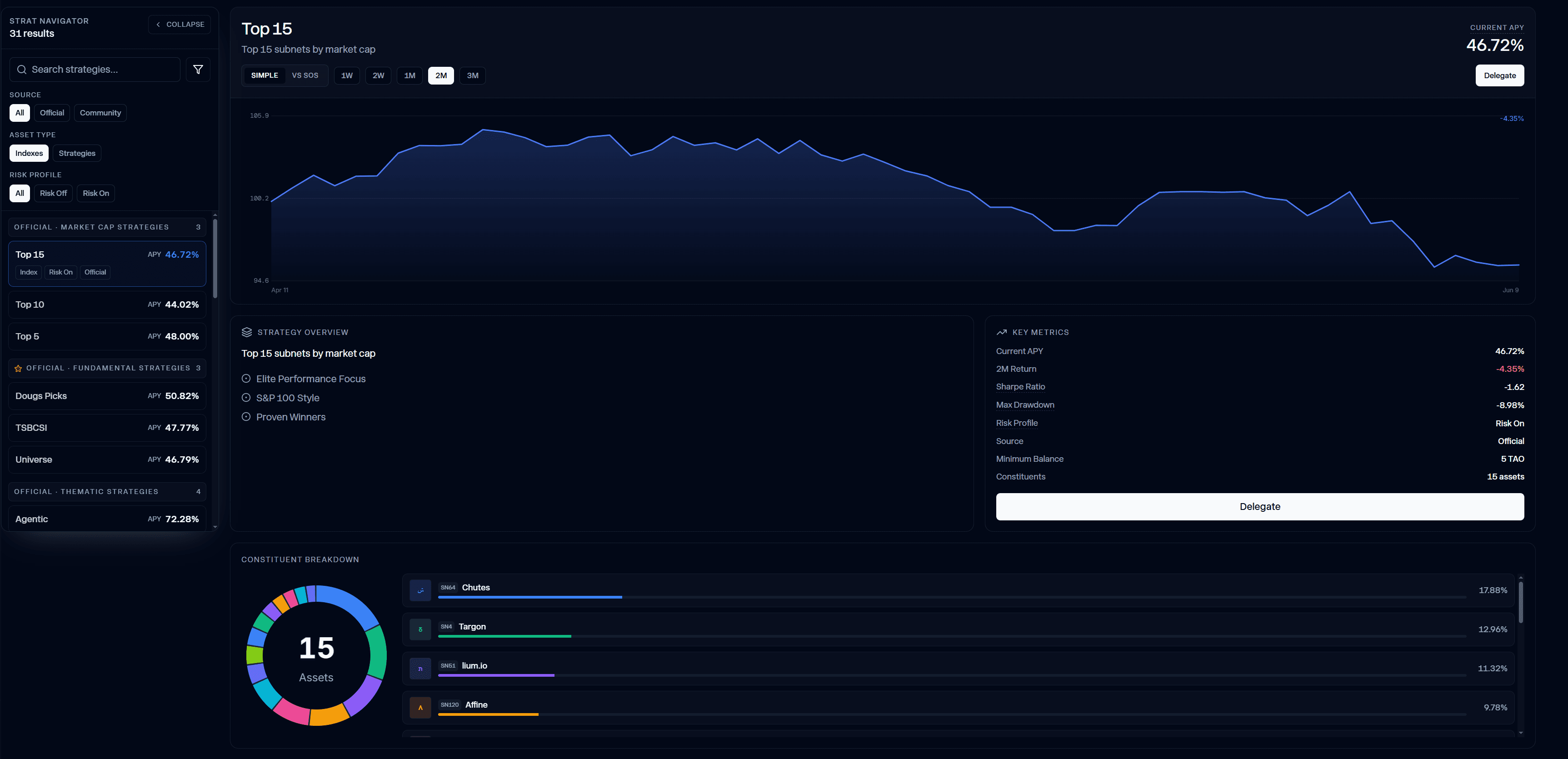

3.2 INDEX PRODUCTS

Picking winning subnets is the primary job in dTAO. For most allocators, the research burden is the binding constraint. Tracking 128 subnets with enough sophistication to make informed decisions is effectively a full-time job that often requires an entire team to execute. That includes evaluating deregistration risk, pool metrics, emissions dynamics, validator behaviour, liquidity conditions, and the underlying fundamentals of each subnet team. The simplest way to reduce that burden is to buy the market via an index rather than pick winners.

Index exposure is available at two levels. Yuma offers two managed funds for accredited investors: a Subnet Composite Fund that holds market-cap weighted positions across all active subnets, roughly a NASDAQ Composite equivalent for the subnet market, and a Large Cap Subnet Fund that concentrates in the top subnets by market cap, closer to a Dow Jones proxy. Both require a $50,000 minimum and a one-year lock-up. Yuma also publishes a Composite Index that tracks the full subnet market with the same weightings used in its Subnet Composite Fund.

For allocators who want a similar form of index exposure without the accreditation requirement, lock-up, or custody handover, TrustedStake offers a non-custodial alternative. The platform was built to collapse the research burden into a single allocation decision. It routes TAO delegation across five pre-built indexes:

Universe Index: broad exposure to 40+ subnets across the network, constructed as an S&P 500-style basket.

Top 5, 10, and 15 Indexes: concentrated positions in the highest market-cap subnets, closer to an S&P 100-style approach without the long tail.

Sector Indexes: focused strategies across AI Innovation, DeFi, Compute, and Agents for investors with a vertical thesis.

Company Indexes: direct exposure to the full subnet portfolio of a single team.

Community Indexes: strategies built by community members spanning day trading, quantitative investing, agentic trading, yield maximization, and more.

Users can also build custom strategies and publish them to the marketplace. Every strategy carries a risk classification: Risk On strategies invest principal directly into subnet alpha tokens, while Risk Averse strategies deploy only the risk-free root yield and leave principal intact.

The platform is built on Bittensor's native Substrate Proxy Pallet, a chain-level primitive implemented directly within the chain runtime itself rather than through smart contracts. A holder adds TrustedStake as a proxy with staking permissions only: it can delegate, rebalance, and rotate validators, but it cannot transfer funds or take custody. The TAO never leaves the holder's wallet, the holder keeps their keys, and the proxy is revocable with no lock-up periods.

On fees, TrustedStake charges a validator-reward share through its CHK validator. The standard rate is 9% of staking yield, not principal. The team reports an effective rate of ~6.62% as of May 2026, which is among the most competitive in the ecosystem. For context, the default validator take on direct Bittensor staking is 18%, though individual validators may set lower rates.

TrustedStake's partner and integration network includes Kraken Institutional, Yuma, TaoStats, Talisman, and SubWallet. As of June 2026, the platform reports $4.7M in AUM across 2,232 nominators. TrustedStake also reports regular third-party audits including work with Distrust; no published report is publicly available.

CLOSING

The investment opportunity in Bittensor has changed significantly over the last five years, from a single OTC token earned through proof-of-work to 128 independently priced AI instruments and a pending spot ETF.

dTAO replaced a structurally broken emission mechanism through onchain governance, without a hard fork or foundation override. The four subnets covered in this report illustrate what dTAO was built for: surfacing external traction in a market where emissions flow to demand, not relationships. SCORE signed enterprise contracts with PwC France, MetaNova has screened 11M molecules with wet lab validation through Onepot AI, Targon trained a private uncensored model for Venice AI, and Vanta turned its first profitable month verified onchain. None of them depend solely on emissions. Their customers and contracts are external to the emission mechanism. All of it happened before a spot ETF existed.

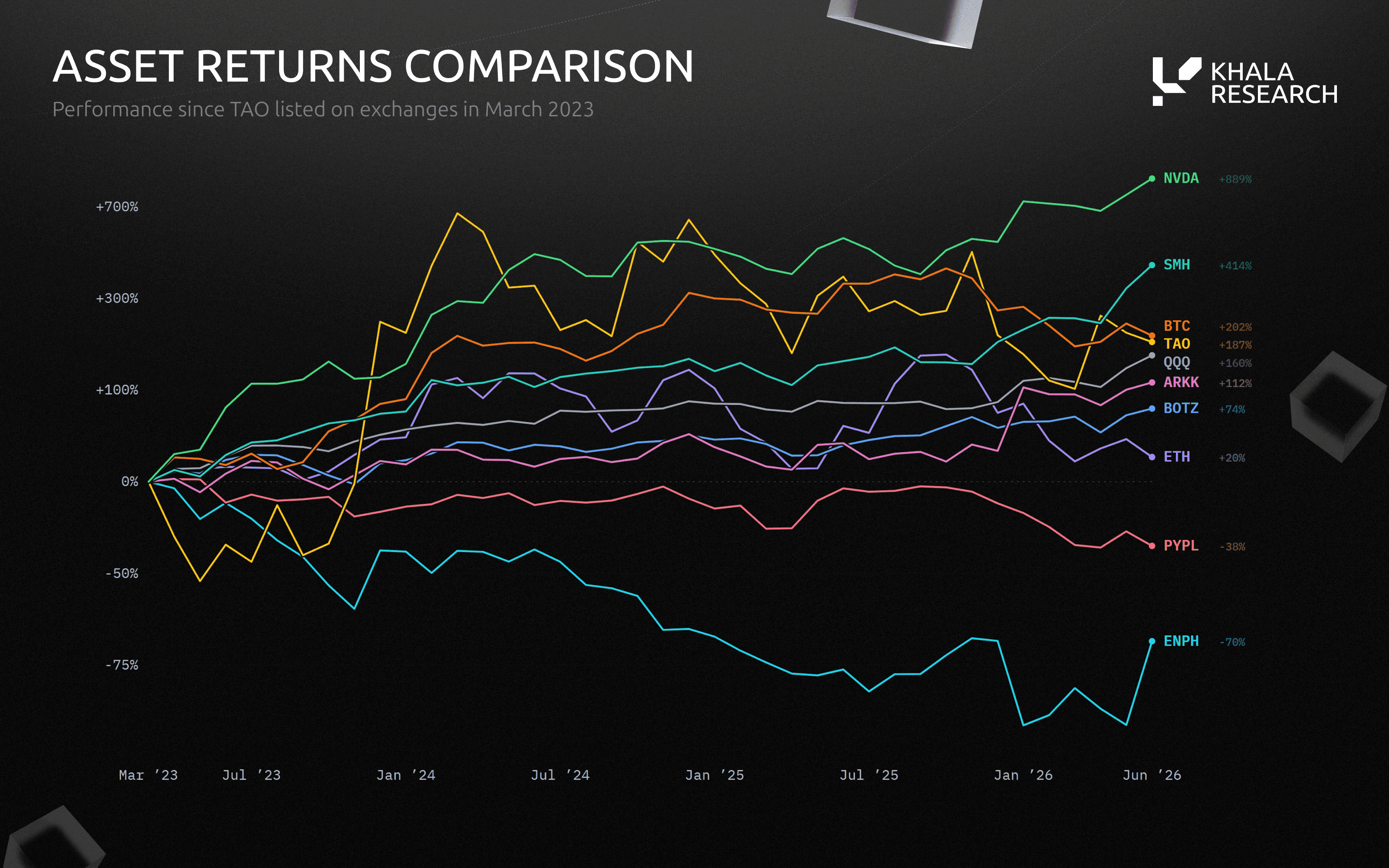

Once TAO listed on exchanges in March 2023, allocators could weigh it against a menu of open-market alternatives. The chart below shows cumulative returns from that date through June 2026.

The chart begins in March 2023, the first date TAO traded on exchanges alongside traditional assets. TAO was the most volatile asset shown, peaking near +700% before correcting to +187%. NVDA produced a stronger terminal return at lower volatility. BTC, SMH, and ETH each delivered positive returns with a smoother path. PYPL and ENPH lost money. The gap between TAO's peak and its endpoint meant the return an allocator actually received depended on when they entered, not on conviction alone.

The ETF S-1 filed on December 30, 2025 brings $144.6T in regulatory assets into range, the same buyer base that delivered $36.6B in net inflows to Bitcoin in its first year of spot access. Grayscale moved from trust launch to S-1 filing in eighteen months; Bitcoin took a decade. That capital does not yet have a TAO allocation pathway, and when it arrives, every onchain holder benefits without owning a wrapper product.

The fight for power in the new AI world may be the most important challenge of our time. Bittensor built the alternative that cannot be closed.